What funding rate arbitrage actually is

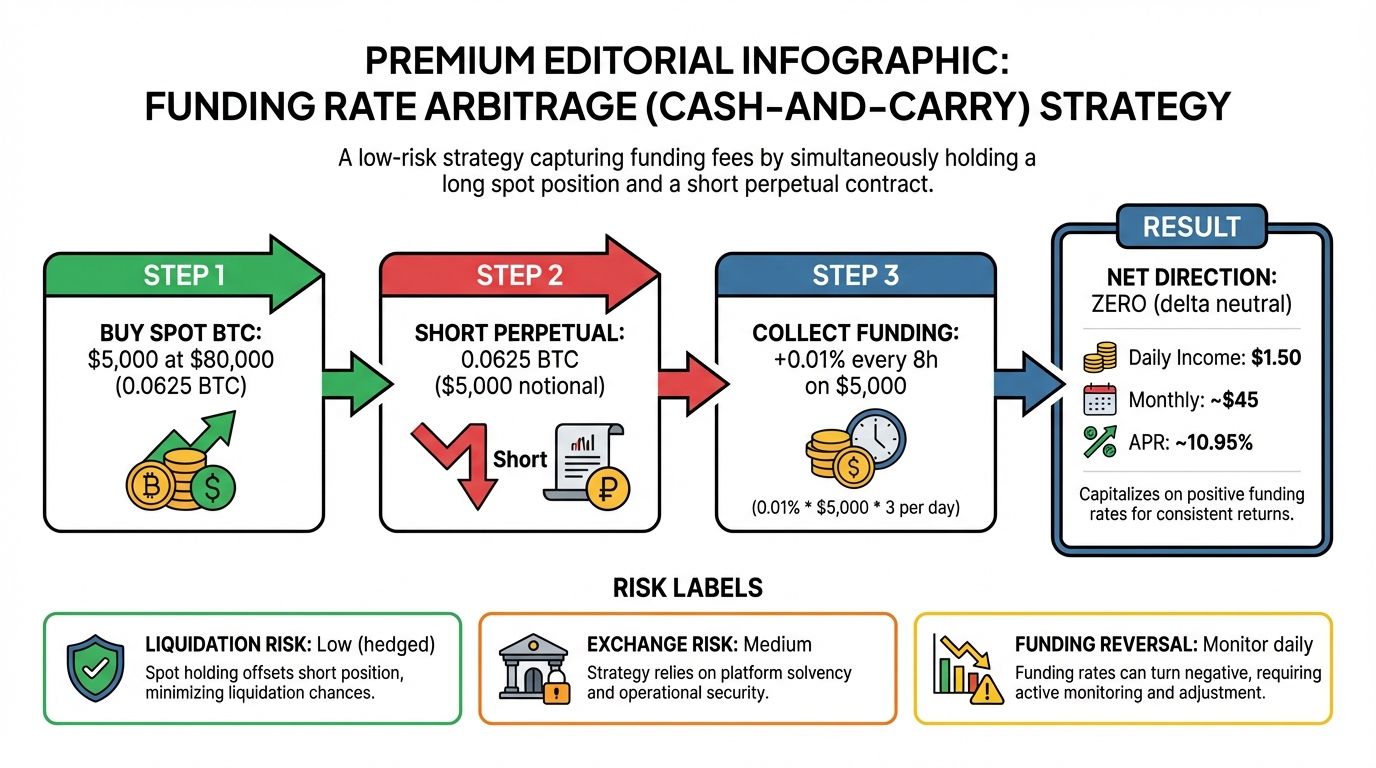

Funding rate arbitrage is a delta-neutral strategy designed to capture yield from the crypto derivatives market without betting on the direction of the asset's price. The mechanism is straightforward: you buy the underlying asset on the spot market and simultaneously short the equivalent notional amount on a perpetual futures exchange. By holding equal and opposite positions, your exposure to price movements cancels out, leaving the funding rate as your primary source of profit or loss.

Perpetual futures contracts were created to keep the futures price close to the spot price. To achieve this, the system uses a funding rate mechanism that periodically transfers payments between long and short traders. When the market is bullish and longs dominate, they pay shorts. When sentiment turns bearish, shorts pay longs. In funding rate arbitrage, you position yourself to be the receiver of these payments, typically by being the short side in a bullish market.

The strategy relies on real-time data tools to identify when funding rates are sufficiently positive to justify the trade. Because the profit margin per funding interval is often thin, success depends on executing the trade efficiently and monitoring the rate closely. While the directional risk is neutralized, the strategy is not risk-free; extreme market volatility can still lead to liquidation if margin requirements are not managed carefully.

How to calculate your real APY

The headline funding rate on a perpetual futures contract is rarely the number that lands in your bank account. It is a gross figure, a theoretical maximum that assumes perfect conditions and zero friction. To find your actual yield, you must annualize the rate and then subtract the costs of execution and holding the position. If you skip this step, you are essentially betting on a profit that doesn't exist.

The foundation of the calculation is simple multiplication. Since most exchanges distribute funding payments every eight hours, there are three payments per day. Over a full year, that compounds to 1,095 payment periods. You can estimate your gross annual percentage rate (APR) by multiplying the current funding rate by 1,095.

However, the gross APR is a misleading benchmark. It ignores the two primary killers of delta-neutral profits: trading fees and slippage. Every time you open your spot and short positions, you pay a maker or taker fee. Every time you rebalance or the price moves significantly, you face slippage. These costs are deducted from the funding payment you receive. If the funding rate is 0.01% per period, your gross APR is roughly 10.95%. But after fees, your net APY could easily drop to 6% or lower, or even turn negative if the market is quiet.

To get an accurate picture, you need to track the net yield in real time. Use a funding rate scanner or exchange dashboard that shows the current rate alongside the estimated APR. Compare this against your specific fee tier on the exchange. If the net yield after estimated fees is less than the risk-free rate or your opportunity cost, the trade may not be worth the capital lock-up. Always calculate the worst-case scenario, not the average.

| Component | Impact on Yield | Mitigation Strategy |

|---|---|---|

| Funding Rate | Positive | Monitor real-time scanners; avoid negative rates |

| Trading Fees | Negative | Use limit orders (maker fees) to reduce costs |

| Slippage | Negative | Execute trades during high liquidity periods |

| Liquidation Risk | Catastrophic | Maintain high margin ratios; use isolated margin |

This table breaks down the variables that determine your final return. The funding rate provides the income, but fees and slippage eat into it. The only way to protect your capital is to manage the liquidation risk, which is the silent threat in delta-neutral strategies. A small price move against your short position can trigger a margin call if you are not careful, wiping out months of funding payments in minutes. Always calculate your real APY before you open the trade.

Spot vs perpetual execution steps

Funding Arb works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

Where to find live yield spreads

Static lists of funding rates are useless for arbitrage. The market moves too fast, and spreads can evaporate or widen by hundreds of basis points between data updates. To capture yield, you need tools that reflect the current state of the perpetual futures market in real time.

Start with a live chart of the funding rate history. This visualizes volatility and mean reversion patterns, helping you distinguish between temporary spikes and structural trends. Watching the chart helps you time your entry when rates are historically high, rather than chasing yesterday’s data.

For precise, actionable numbers, use dedicated arbitrage scanners and data aggregators. These platforms calculate the net basis—the difference between the spot price and the perpetual futures price—adjusted for fees and financing costs. Look for tools that offer real-time data feeds from multiple exchanges, as spreads vary significantly between platforms.

The most reliable data sources are those that pull directly from exchange APIs or provide transparent methodology for their calculations. Avoid platforms that rely on delayed or aggregated data without clear sourcing. When evaluating opportunities, always cross-reference the displayed spread with the exchange’s current fees and liquidity depth to ensure the theoretical yield translates into actual profit.

Risks that can liquidate your position

Funding rate arbitrage is often marketed as a risk-free yield source, but that label ignores the mechanics of leverage. While you are delta-neutral—meaning spot gains offset futures losses—you are not immune to price volatility. In fact, extreme price movements are the primary threat to your capital. If the market spikes, the short side of your position can be liquidated before the spot side has time to adjust, leaving you with a net loss.

The most immediate danger is a rapid price spike. When the underlying asset surges, your short futures position requires additional margin to maintain the leverage ratio. If you cannot deposit more collateral quickly enough, the exchange will liquidate your short. This event is catastrophic because you lose the short position while still holding the spot asset, effectively destroying the hedge. It is similar to a car braking system failing: the longer you drive at high speed, the more likely the brakes will overheat and fail.

Beyond liquidation, exchange insolvency remains a persistent risk in crypto. Unlike traditional bank accounts, crypto holdings on centralized exchanges are not insured by government bodies like the FDIC. If an exchange fails, your spot and futures balances could be frozen or lost entirely. This risk is compounded by the fact that you are splitting your capital across two platforms or one platform’s isolated margin accounts.

Finally, the strategy assumes funding rates remain positive. While they are often positive in bull markets, they can turn negative during bear markets or periods of extreme short interest. In these scenarios, you are paying the funding rate rather than receiving it. This transforms your "yield" into a continuous cost, potentially eating into your principal if the negative rate persists for multiple 8-hour intervals. Always monitor real-time data tools to detect these shifts before they impact your P&L.

Common questions about funding arb

How to do funding rate arbitrage?

Funding rate arbitrage leverages the perpetual futures mechanism by taking a delta-neutral position. You buy the asset on the spot market and simultaneously sell (short) the equivalent notional amount on a perpetual futures exchange. By taking both sides of the transaction, you effectively cancel out your price risk, allowing the funding rate to become your primary source of return.

What is a funded arbitrage?

Funded arbitrage is a strategy to collect funding payments from the crypto futures market without taking on directional price risk. You hold equal and opposite positions in spot and perpetual futures. Because price movements cancel out, the periodic funding payments—made by longs to shorts when rates are positive—become your profit and loss (P&L) driver.

Is funding rate arbitrage profitable?

Funding rate arbitrage can provide stable income, but it carries risks. In extreme situations, when prices spike in either direction, there is a risk of liquidation for the futures side of the position. While the strategy is designed to be market-neutral, maintaining sufficient margin and monitoring funding rates in real-time are essential to protect your capital.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!