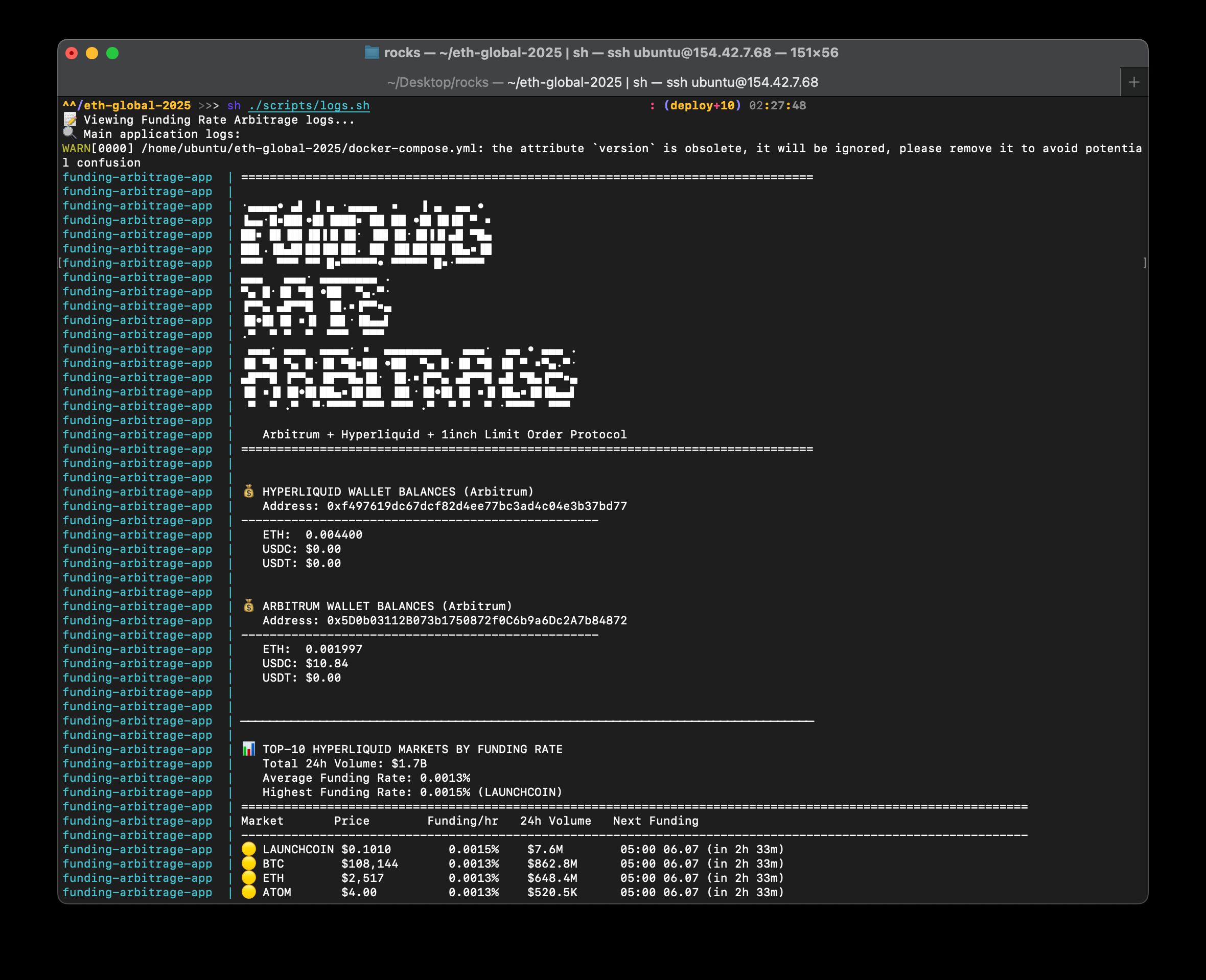

How funding rate arbitrage works

Funding rate arbitrage is a delta-neutral strategy that allows traders to earn returns from the periodic payments exchanged between long and short positions in perpetual futures contracts. Unlike directional trading, where profit depends on the asset's price moving up or down, this approach isolates the funding fee as the sole source of return.

The mechanism relies on the price convergence between spot and perpetual futures markets. Perpetual contracts do not have an expiry date, so exchanges use a funding rate to tether the futures price to the underlying spot price. When the market is bullish, longs pay shorts. When bearish, shorts pay longs.

To capture positive funding payments, a trader executes a two-leg trade: buying the asset on the spot market (long) while simultaneously opening an equal-sized short position on the perpetual futures market. This creates a hedged, or "delta-neutral," portfolio. If Bitcoin's price rises, the profit on the spot holding is offset by the loss on the short futures position, and vice versa. The net exposure to price movement is effectively zero.

The profit comes exclusively from the funding payment. In a typical market with positive funding rates, the short futures position receives a payment from the long futures position every eight hours (or whatever interval the exchange dictates). Since the trader is short on futures and long on spot, they collect these payments while their principal remains protected from market volatility.

This strategy functions similarly to borrowing at a low interest rate and lending at a higher one. The "spread" is the funding rate. While the returns are often modest compared to leveraged directional trades, the risk profile is fundamentally different, as it removes the threat of liquidation from sudden price spikes, provided the exchange's margin requirements are met.

Choosing the right exchange infrastructure

Funding rate arbitrage relies on capturing the periodic payments between perpetual futures and spot markets. To make this work, you need a setup that minimizes friction. The biggest threats to your spread are slippage, high fees, and counterparty risk. Your choice of infrastructure dictates how much of the funding rate you actually keep.

Centralized vs. Decentralized Exchanges

Centralized exchanges (CEXs) like Binance or Bybit offer deep liquidity and tight spreads, which are essential for entering and exiting positions without moving the market. Decentralized exchanges (DEXs) provide non-custodial control but often suffer from fragmented liquidity and higher gas costs, which can eat into your profits. For most arbitrageurs, a hybrid approach works best: using a CEX for the high-volume futures leg and a DEX or another CEX for the hedging leg.

Liquidity and Slippage

Deep order books are non-negotiable. If your position size is large relative to the order book depth, slippage will destroy your edge. Always check the top-of-book liquidity before executing. A thin market might show a high funding rate, but the cost to enter the trade could be higher than the expected yield.

Counterparty Risk

On a CEX, you rely on the exchange to honor your positions and payouts. On a DEX, you rely on smart contract security. Both carry risks. Diversifying across multiple platforms can mitigate the impact of a single point of failure, but it also increases operational complexity.

| Feature | Centralized Exchange (CEX) | Decentralized Exchange (DEX) |

|---|---|---|

| Liquidity | Deep, consolidated order books | Fragmented, often lower depth |

| Fees | Low trading fees, no gas | Gas fees + protocol fees |

| Counterparty Risk | Exchange insolvency/custodial | Smart contract bugs/hacks |

| Speed | High throughput, instant settlement | Variable, depends on block time |

Technical Analysis Setup

Before committing capital, analyze the funding rate trends and price action. Use a technical chart to identify stable funding rates and avoid assets with extreme volatility that might signal underlying market stress.

Reading the spread for sustainable yield

Identifying a viable funding arb opportunity starts with distinguishing between a structural premium and a fleeting spike. A temporary rate surge often signals a short squeeze or a single large position unwinding, which typically collapses within hours. Sustainable yield, however, requires a consistent positive spread over a longer horizon, indicating a genuine imbalance between long and short interest in the market.

To filter for these lasting opportunities, you need to look beyond the current 8-hour rate. Examine the 30-day average and the historical distribution of rates for specific tokens. If a token consistently trades at a premium during market volatility but remains neutral during calm periods, it may offer a more predictable cash flow than a token with erratic, day-to-day fluctuations.

Data tools from providers like Amberdata and HangukQuant Research emphasize that robust data is key to navigating these subtleties. By tracking the spread across multiple exchanges, you can identify where the inefficiency is deepest and most persistent. This granular view helps you avoid entering positions where the spread is likely to mean-revert before your funding payments accumulate.

The chart below illustrates the volatility of ETH funding rates over the last 30 days. Notice how sharp spikes often precede a rapid return to the mean. Trading the average rather than the peak is a more reliable strategy for capturing steady yield.

Managing Liquidation and Basis Risk

Funding arbitrage is often marketed as a "risk-free" yield strategy, but that label ignores two very real threats: basis risk and liquidation risk. If you ignore these, a profitable funding rate can quickly vanish under the weight of adverse market moves.

Basis Risk: When the Spread Closes

Basis risk arises from the divergence between the spot price of an asset and its perpetual futures price. In a perfect arbitrage scenario, you buy spot and short futures, collecting the funding rate while the spread remains stable. However, if the market turns sharply, the spread can widen against you.

For example, if the crypto market crashes, your short futures position might gain value, but your spot holdings lose value. If the basis widens negatively (the futures price drops significantly below spot), the mark-to-market losses on your short can exceed the funding payments you’ve collected. This is not just theoretical; during high-volatility events, basis spreads can swing wildly, eroding margins in hours rather than weeks.

Liquidation Risk: The Margin Call Trap

Liquidation risk is the more immediate danger. Perpetual futures are leveraged instruments. If the price of the underlying asset moves against your short position, your margin balance decreases. Exchanges have maintenance margin requirements; if your equity falls below this threshold, the exchange will liquidate your position to cover the loss.

This risk is amplified by the nature of funding payments. While positive funding rates add to your margin (a benefit), negative funding rates deduct from it. If you are caught in a squeeze where you must pay funding while simultaneously losing on the price move, your margin depletes twice as fast. A sudden 5% drop in spot price can trigger a liquidation if your leverage is not carefully managed, wiping out months of accumulated funding yield.

Hedging the Unpredictable

To mitigate these risks, traders often use dynamic hedging techniques. This might involve adjusting the size of the spot or futures position as volatility increases. Some sophisticated strategies use options to cap downside risk, effectively buying insurance against a market crash.

Monitoring live market data is essential. Keeping an eye on the basis spread and your margin ratio in real-time allows you to exit or rebalance before a liquidation event occurs. The goal isn't to eliminate risk entirely—that's impossible in leveraged markets—but to ensure that the funding yield compensates adequately for the volatility you are exposed to.

How to execute a funding arbitrage trade

Executing a funding rate arbitrage requires precision. The strategy hinges on maintaining a delta-neutral position: you hold a spot asset while shorting the equivalent amount in perpetual futures. This structure isolates the funding payment as your primary source of return, removing directional market risk.

1. Select a high-yield asset

Start by identifying a perpetual contract with a consistently positive funding rate. Use a data provider to filter for assets where the rate remains above the annualized risk-free rate. Look for stability rather than spikes; you want a reliable stream of income, not a one-time anomaly.

2. Open the spot position

Purchase the underlying asset on the spot market. Ensure the exchange supports the same ticker for both spot and futures to avoid basis confusion. This asset forms the long side of your hedge and will generate the funding payments you aim to capture.

3. Short the futures contract

Simultaneously open a short position in the perpetual futures market for the exact same quantity of the asset. This short position offsets the price movement of your spot holding. If the market drops, your short profits; if it rises, your spot gains. The net exposure to price is zero.

4. Monitor and rebalance

Funding rates are paid every eight hours on most major exchanges. Check your position regularly to ensure the short size matches the spot holding. If the market moves significantly, your hedge may become unbalanced. Rebalance by buying or selling the spot asset to maintain neutrality.

Common questions about funding arb

How to do funding rate arbitrage?

The core mechanic is straightforward: borrow capital at a low interest rate and invest it where it generates higher returns through perpetual swap funding fees. Success requires rigorous market research to identify tokens with consistently positive funding rates. You must analyze historical data to ensure the rate persists long enough to cover borrowing costs and generate a net profit.

Is arbitrage possible for beginners?

Pure arbitrage in highly efficient markets like the New York Stock Exchange is nearly impossible for retail traders due to institutional speed advantages. However, cryptocurrency perpetual markets remain less efficient, offering occasional opportunities for those who understand the mechanics. Beginners can participate by focusing on established pairs and using reliable data sources to track funding rates.

Do I need a large capital base?

While larger capital allows for better diversification across multiple positions, funding arbitrage can be attempted with smaller amounts. The key is selecting assets with high enough funding rates to offset trading fees and slippage. Many traders start with a single position to understand the execution risks before scaling up.

What are the main risks?

The primary risk is not price direction but funding rate volatility. If the market sentiment shifts, funding rates can turn negative, eroding profits or creating losses. Additionally, exchange-specific risks like withdrawal delays or account freezes can trap capital. Always monitor your positions and maintain sufficient margin to avoid liquidation during sudden market moves.

No comments yet. Be the first to share your thoughts!