Funding arbitrage limits to account for

Funding rate arbitrage is a constrained mechanical trade, not passive income. It relies on capturing the spread between perpetual swap funding rates while holding an offsetting spot position. In 2026, the primary constraint is infrastructure: managing basis risk across multiple venues with varying latency and fee structures.

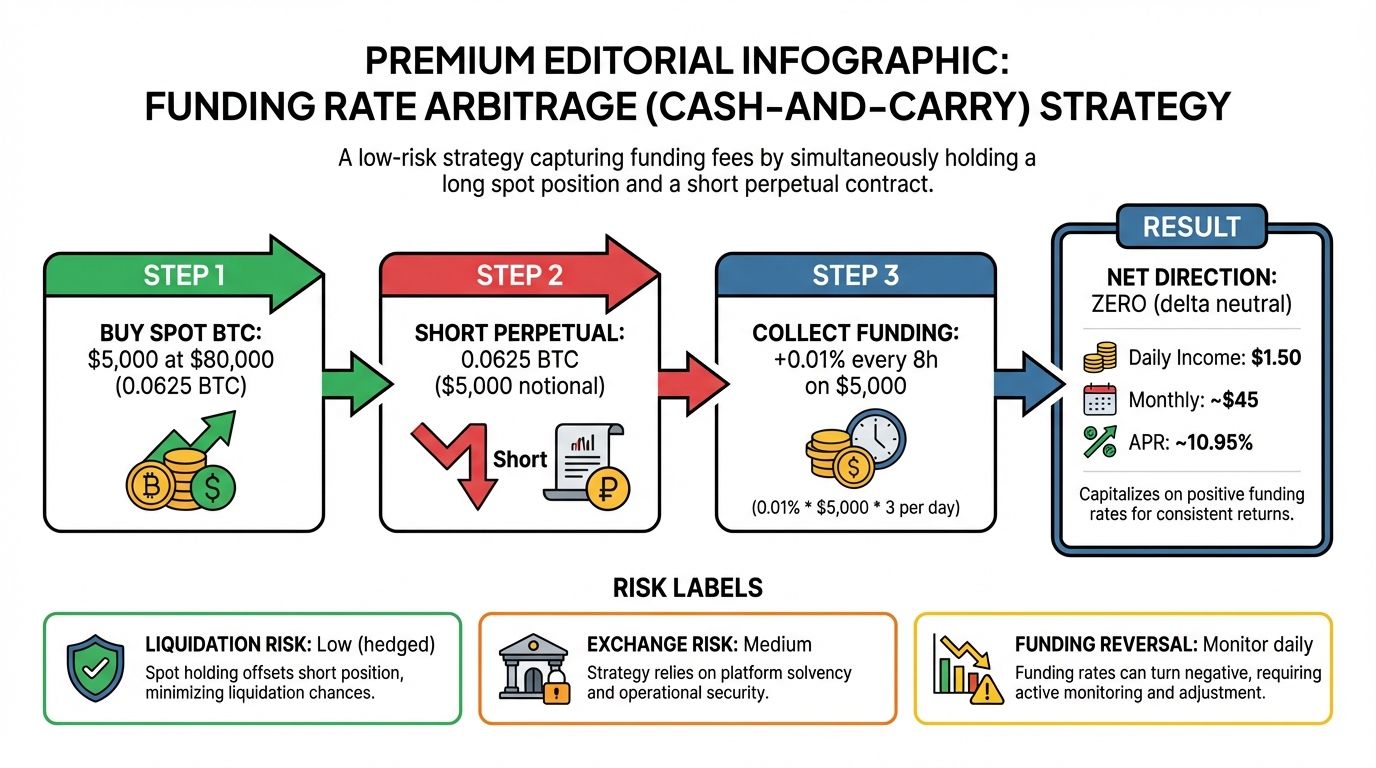

The core mechanic involves going long spot and shorting perpetuals (or vice versa) to harvest periodic payments. Profitability hinges on the net yield after fees, exchange latency, and funding interval alignment. A positive funding rate does not guarantee profit if the basis converges unfavorably or if exchange maintenance margins shift unexpectedly.

Infrastructure shifts have tightened these margins. Exchanges now offer varying funding intervals and dynamic rate caps, which can turn a stable arb into a volatile position overnight. Traders must monitor real-time funding data to ensure the spread remains wide enough to cover transaction costs and potential liquidation risks.

Liquidation risk remains the most significant threat. A sharp market move against your spot position can expose you to losses if the perpetual hedge does not offset them immediately due to funding delays or margin requirements. This asymmetry creates tail risk that can wipe out months of accumulated funding yields in a single event.

Funding arbitrage choices that change the plan

Funding rate arbitrage is often described as a "yield-free" strategy because it involves holding equal and opposite positions. In theory, price movements cancel each other out, leaving only the net funding rate as profit. In practice, concrete factors like spread costs, exchange risk, and margin management can erode that yield or introduce unexpected costs.

Execution and Spread Costs

The most immediate drag on profitability is the spread between entry and exit prices. Even if hedged, you pay the spread twice: once when opening the long position and once when opening the short. If the funding rate is 0.01% per 8 hours (0.03% daily), but your round-trip spread cost is 0.05%, you start the trade with a negative yield.

Account for trading fees carefully. Some exchanges offer fee rebates or maker discounts for high-volume traders, while others charge taker fees that can outweigh funding income. Calculate your expected annualized percentage yield (APY) by subtracting these friction costs. If the net APY after fees is less than 5-10%, the trade may not be worth the operational overhead compared to simpler yield farming options.

Exchange Risk and Counterparty Exposure

Unlike non-custodial DeFi strategies, funding arb typically requires centralized exchanges (CEXs), introducing counterparty risk. If one exchange experiences a liquidity crunch, hack, or withdrawal freeze, your hedge may fail. For example, if the exchange where you hold the short position halts withdrawals, you cannot rebalance if the market moves violently against you.

Consider the regulatory environment as well. Exchanges in different jurisdictions may face sudden compliance changes that restrict access. Diversifying across multiple reputable platforms mitigates this but increases the complexity of managing capital across different interfaces and security protocols.

Liquidation and Margin Management

While positions are hedged, they are not immune to liquidation if margin is not managed correctly. If one side incurs significant losses (e.g., your long position drops sharply while your short gains), you may need to add margin to that specific leg to avoid liquidation. Without sufficient capital, you could be forced to close the losing position, leaving you exposed.

Volatility spikes can trigger margin calls if leverage is too high. Maintain a healthy margin ratio and monitor funding rates closely. A sudden shift in market sentiment can cause funding rates to flip from positive to negative, turning your income stream into a cost.

| Factor | Impact on Yield | Mitigation Strategy |

|---|---|---|

| Trading Spreads | High initial drag | Use limit orders and high-volume pairs |

| Exchange Fees | Moderate to high | Negotiate maker/taker rates or use fee rebates |

| Counterparty Risk | Catastrophic loss | Diversify across top-tier CEXs |

| Margin Calls | Position closure | Maintain low leverage and high margin ratio |

Choose the next step

Funding rate arbitrage is a mechanical process requiring precise execution. To turn this strategy into a reliable yield source, establish a rigid operational framework. The following steps outline how to structure, execute, and manage arbitrage positions.

Look for consistent, positive funding rates on long-dated futures contracts. A single spike is noise; a sustained divergence across multiple periods indicates a structural imbalance you can exploit. Use data platforms like Coinglass or Amberdata to track these trends over 24-72 hour windows.

Subtract trading fees, withdrawal costs, and exchange spreads from the gross funding rate. A 0.05% funding payment often evaporates after a 0.04% round-trip fee. Only proceed if the net annualized percentage yield (APY) exceeds your risk threshold, typically aiming for 10-20% APY or higher to justify the operational effort.

Open a long spot position and an equal-value short perpetual futures position simultaneously. This hedges your exposure to underlying asset price movements. If Bitcoin rises, your spot gains while your short loses, keeping your portfolio value stable while you collect the funding payments from the short side.

Even delta-neutral strategies face liquidation risk if the exchange’s margin requirements shift or if funding rates reverse sharply. Set tight stop-losses on the short leg and maintain excess margin buffers. Regularly check the maintenance margin requirements on your chosen exchange to prevent forced liquidations during volatile market swings.

Funding rates change with market sentiment. Manually tracking dozens of pairs is inefficient. Use bots or scheduled scripts to rebalance your positions every 8 hours (standard funding interval) or daily. Automation ensures you capture payments promptly and adjust hedge ratios as the market evolves.

Spotting Weak Funding Arbitrage Options

Not every positive funding rate signals a viable trade. Many retail traders chase high percentages without checking the underlying market structure, leading to losses. A high rate often reflects genuine short-squeezes or low liquidity rather than a sustainable spread between exchanges.

The Cross-Exchange Illusion

Classic cross-exchange arbitrage assumes you can capture the delta between two venues. However, if one exchange pays +0.05% and another charges +0.08%, the net is negative. This often happens on newer or less liquid platforms like Hyperliquid where rates spike artificially. You must calculate the net yield after fees, not just the raw rate differential.

Ignoring Liquidation Risk

Funding arbitrage requires maintaining a delta-neutral position, typically by holding spot and shorting futures. If the market moves sharply against your short, you face liquidation risk. A small price spike can wipe out months of funding income. Always check the maintenance margin requirements and current leverage levels on both sides of your trade.

Hidden Fee Drag

Withdrawal fees, deposit times, and trading fees can turn a profitable-looking spread into a loss. If you need to rebalance positions frequently to manage risk, these costs compound quickly. Use the

to track current volatility, but remember that fees are static while rates fluctuate.Low Liquidity Traps

High funding rates on low-volume pairs are often traps. Market makers may be unwilling to provide deep liquidity, causing rates to swing wildly. This makes it difficult to enter or exit positions without significant slippage. Stick to major pairs with deep order books to ensure you can execute your hedge at fair prices.

Funding arb: what to check next

Funding rate arbitrage remains a popular strategy for yield optimization, but it comes with specific mechanical and market risks. Before deploying capital, it helps to understand exactly how the trade executes and where the profit margins actually live.

No comments yet. Be the first to share your thoughts!