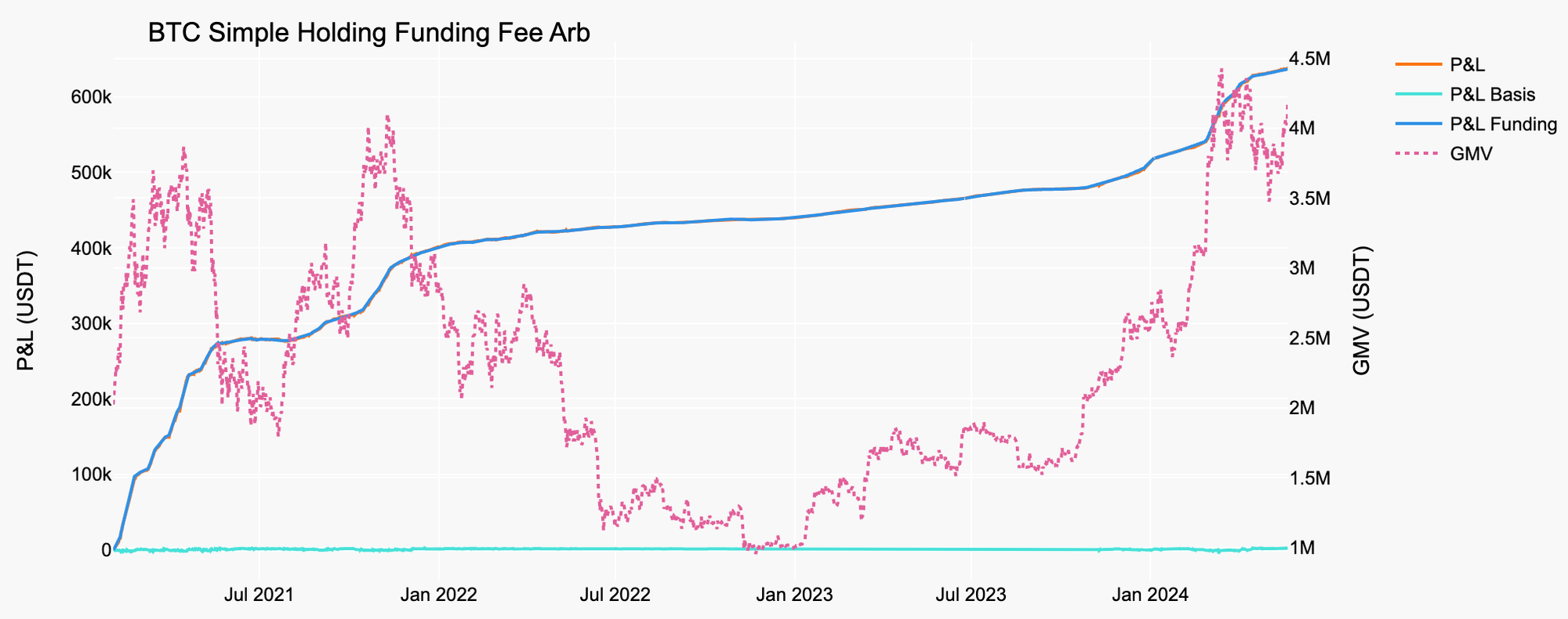

How funding rate arb works

Funding rate arbitrage is a delta-neutral strategy designed to capture the spread between spot and perpetual futures markets without taking on directional price risk. The mechanism relies on a simple premise: if perpetual futures trade at a premium or discount to the spot price, traders can lock in that difference by holding equal and opposite positions in both markets.

To execute this trade, you buy the asset on the spot market while simultaneously shorting the equivalent notional amount on a perpetual futures exchange. This pairing creates a delta-neutral portfolio. If the price of Bitcoin moves up, the gain in your spot position is offset by the loss in your short futures position, and vice versa. The price volatility cancels out, leaving you exposed only to the funding rate payments.

Perpetual futures contracts use a funding rate mechanism to tether the contract price to the underlying spot price. This rate is exchanged between long and short traders at regular intervals—typically every eight hours. When the market is bullish, longs pay shorts; when it is bearish, shorts pay longs. In a funding rate arbitrage setup, you hold the short futures position specifically to collect these payments from the long traders.

The profitability of this strategy depends on the funding rate remaining favorable relative to your costs. As noted by industry analyses, the annualized return is calculated by multiplying the funding rate per period by the number of periods in a year [1]. However, the strategy is not without risk. Extreme market moves can trigger liquidation on the futures side if margin is insufficient, even if the overall portfolio remains theoretically neutral [2]. Success requires precise execution and robust risk controls to manage these leverage-related vulnerabilities.

Calculating Net Yield After Fees

To understand the real profitability of funding rate arbitrage, you need to look past the headline numbers. The gross funding rate is just the starting point. The actual return you keep depends on how efficiently you execute the trade and how much you pay in overhead. If your fees eat up the spread, the strategy stops being an income stream and becomes a liability.

The formula for the gross annualized rate is straightforward: multiply the funding rate per period by the number of funding intervals in a year. For example, if a funding rate is 0.01% every eight hours, there are three payments per day and 1,095 per year. $0.01% \times 1,095$ gives you a gross APR of roughly 10.95%. However, this number assumes you pay zero fees, which never happens in practice.

Your net yield is the gross rate minus the costs of maintaining the delta-neutral position. These costs include taker fees for opening and closing positions, slippage from market impact, and the funding payments you make if the rate flips negative. In a typical scenario, you buy the asset on the spot market and short it on the perpetual futures exchange. If both sides incur a 0.05% fee, your total transaction cost is 0.10% per cycle. Over a year, these costs compound and significantly reduce your final return.

Slippage is another hidden cost that often gets overlooked. When you enter large positions, the market moves against you. A poorly timed entry can add another 0.05-0.10% to your costs. Over many cycles, this adds up. Automation helps here by executing trades at optimal times, but it doesn't eliminate market impact entirely.

To see how different fee structures impact your bottom line, compare the net yields across various scenarios. This table shows how fees and slippage affect a baseline 12% gross APR.

| Scenario | Gross APR | Total Fees & Slippage | Net APR |

|---|---|---|---|

| Low Cost Exchange | 12.0% | 2.5% | 9.5% |

| Standard Exchange | 12.0% | 5.0% | 7.0% |

| High Slippage | 12.0% | 8.0% | 4.0% |

The difference between a 9.5% net return and a 4.0% net return is substantial. It determines whether you are building a sustainable income stream or just breaking even. Focus on minimizing fees through maker orders and limiting slippage with careful position sizing. These operational details are what separate successful arbitrageurs from those who simply chase high gross rates.

Setting up automated execution

Manual execution rarely survives the reality of funding rate arbitrage. Even with a perfectly hedged delta-neutral position, the spread between spot and perpetual funding rates can shift in seconds. If you are relying on manual rebalancing or waiting for a human to notice a rate spike, you are leaving money on the table or exposing your short leg to liquidation risk.

Automated infrastructure is not a luxury here; it is the core engine of the strategy. Your bots must handle three critical tasks: identifying viable spreads, executing the paired trades simultaneously, and rebalancing as funding rates fluctuate. This requires low-latency API connections to multiple exchanges and a robust monitoring system that tracks funding intervals—typically every eight hours.

Use API keys with the minimum necessary permissions. Enable IP whitelisting to prevent unauthorized access. Store your secrets in environment variables, never in your codebase. Most exchanges offer testnets; use them to verify your connection stability before committing real capital.

Build a script that polls the funding rate endpoint across your target exchanges. Filter for pairs where the spread exceeds your threshold (e.g., annualized > 15%). Use a TechnicalChart to visualize historical spikes and set realistic expectations for volatility.

When a spread is detected, trigger a single transaction that opens a long position on the spot market and a short position on the perpetual futures market. The notional amounts must be equal to maintain delta neutrality. If the exchange APIs support it, use atomic order groups to reduce the risk of one leg failing while the other succeeds.

Set up a cron job to check your positions before each funding interval. If the funding rate has flipped or dropped below your profit threshold, close the positions. Collect the funding payment and repeat the cycle. Manual collection is prone to human error; let the bot handle the transfer of funds from the futures wallet to your spot wallet.

This infrastructure transforms funding arbitrage from a sporadic, high-effort activity into a scalable system. By removing emotional decision-making and manual delays, you capture the full value of the funding rate spread while maintaining strict risk controls.

Managing liquidation and basis risk

The theoretical safety of a delta-neutral position relies on continuous rebalancing. In practice, sharp market moves can trigger liquidation before the system has time to adjust. When the short leg faces a sudden rally, the exchange’s margin engine may force a liquidation if the available margin falls below the maintenance requirement. This is not a failure of the strategy’s logic, but a failure of the infrastructure’s speed and capital efficiency.

Liquidation risk is highest when volatility spikes faster than the rebalancing frequency. If you are holding a short perpetual futures position, a rapid price increase erodes your margin balance. Without automated safeguards, manual intervention is often too slow. The difference between a profitable hedge and a blown account is usually the latency of your risk management tools.

Basis risk introduces a different layer of uncertainty. The funding rate is not static; it fluctuates based on market sentiment. If the basis converges against you, the income stream dries up or turns negative. This can happen when the market shifts from bullish to bearish, causing funding rates to drop or even flip. While this does not trigger liquidation, it erodes the profitability of the trade.

To manage these risks, you need more than just capital; you need automation. Real-time monitoring of margin ratios and automatic rebalancing are non-negotiable for high-frequency funding arbitrage. Without these, you are exposed to the very directional risks you are trying to hedge.

Validating arb infrastructure performance

Delta-neutral funding arbitrage looks clean on paper, but infrastructure friction eats margins. A setup that ignores latency, fee accounting, and exchange solvency is just a slow liquidation event waiting to happen. Before committing capital, you need a rigorous audit checklist for your execution stack.

Latency and Execution Checks

Speed determines whether you capture the spread or get rekt by slippage. Your infrastructure must handle simultaneous spot buys and perpetual shorts with minimal lag. Test your API response times under load and verify that your order routing doesn't introduce delays. If your execution isn't near-instant, the funding rate differential you're chasing might vanish before your position is live.

Fee Accounting

Fees are the silent killer of arb strategies. You must account for trading fees (maker/taker), funding payments, and withdrawal/deposit costs. A common mistake is ignoring the impact of taker fees on your initial entry. Run a backtest that includes realistic fee assumptions for both legs of the trade. If your projected annualized yield is less than 2-3x the total fee burden, the trade is likely not worth the operational risk.

Exchange Solvency Monitoring

You are effectively lending money to the exchange when you hold a perpetual futures position. If the exchange becomes insolvent, your collateral is gone. Monitor on-chain reserves and exchange audit reports. Diversify your positions across multiple reputable venues to mitigate counterparty risk. Never put all your capital on a single platform, no matter how strong their marketing looks.

Common questions about funding arb

Funding rate arbitrage is often misunderstood as a "guaranteed profit" machine. It is a mechanical strategy that requires precise execution and constant monitoring. Below are the most frequent questions regarding delta-neutral execution and risk controls.

No comments yet. Be the first to share your thoughts!