Funding arbitrage strategy limits to account for

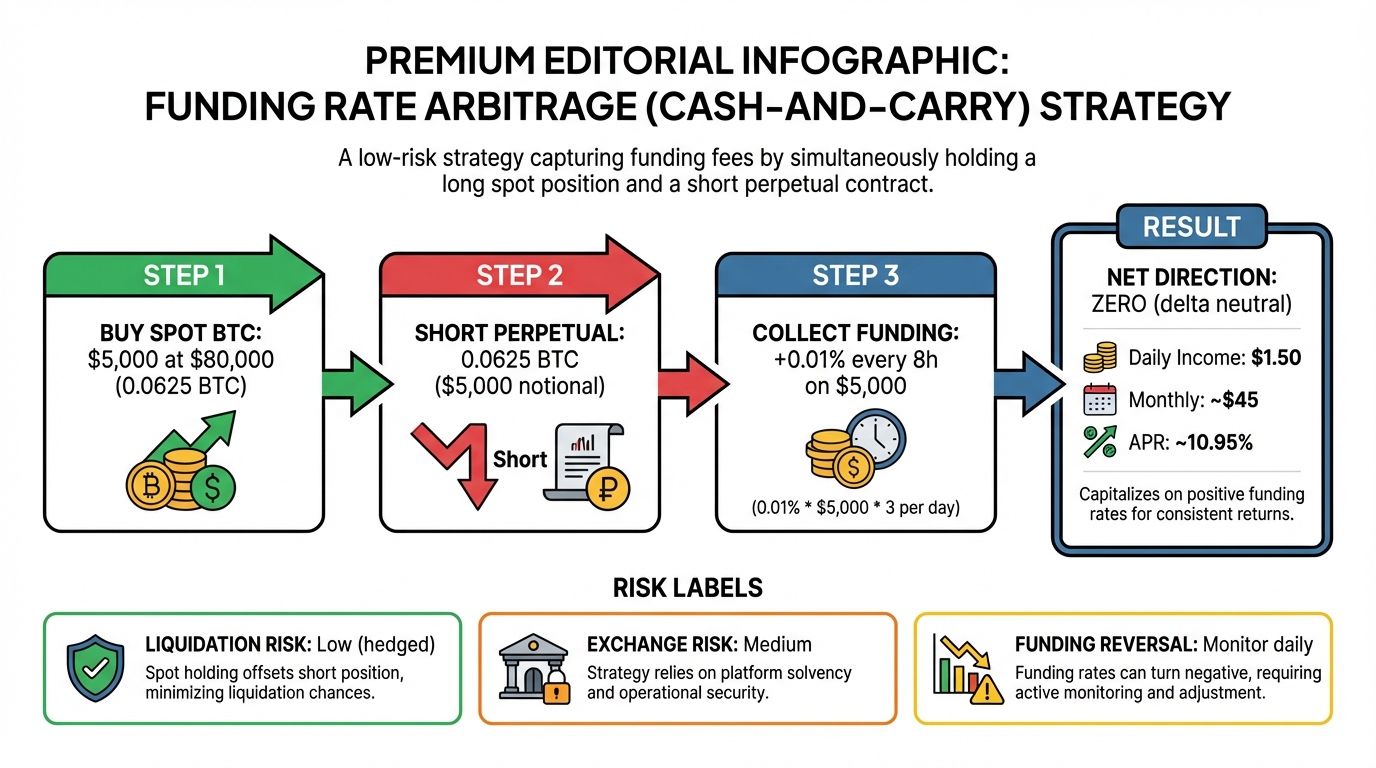

Funding rate arbitrage involves taking opposing positions on the same asset across different exchanges to capture the periodic funding fee. Typically, a trader holds a long position on an exchange with negative or low funding rates and a short position on an exchange with positive rates. The goal is to earn the spread between these payments while maintaining a market-neutral delta.

However, this strategy is not risk-free. The primary constraint is the basis risk between exchanges. If the price divergence between the two platforms widens unexpectedly, the exchange offering the higher funding rate may suffer a larger drawdown, requiring additional margin. Also, platform-specific risks such as withdrawal freezes or liquidity gaps can trap capital precisely when rebalancing is most critical.

Success depends on infrastructure speed and capital efficiency. Traders must monitor real-time funding data and maintain sufficient liquidity to cover sudden margin calls. Without robust tools to track these variables, the theoretical yield often disappears into execution slippage and unexpected volatility.

Funding arb strategy choices that change the plan

Funding rate arbitrage seeks to capture the spread between long and short funding payments on perpetual futures. While the core mechanic is straightforward—go long on an exchange with negative funding and short on one with positive funding—the execution introduces specific frictions. The strategy’s profitability depends less on market direction and more on the stability of these spreads and the reliability of the infrastructure connecting them.

Before committing capital, evaluate the following operational factors. These tradeoffs determine whether the strategy generates consistent yield or erodes under operational drag.

| Factor | Centralized Exchanges | Decentralized Protocols | Impact on Yield |

|---|---|---|---|

| Funding Payment Speed | Every 8 hours | Every 8 hours or per block | CME-style delays can miss spread windows; on-chain immediacy captures volatility. |

| Counterparty Risk | High (exchange solvency) | Low (smart contract dependent) | Exchange insolvency wipes out principal; smart contract risk is limited to protocol layer. |

| Slippage & Fees | Low (high liquidity) | Variable (AMM depth) | High slippage on DEXs can erase the funding rate premium entirely. |

| Execution Complexity | Simple (UI-based) | High (bridge + tx) | Manual bridging introduces latency and gas costs that reduce net APR. |

The choice between centralized and decentralized venues hinges on your risk tolerance. Centralized exchanges offer deep liquidity and low fees, but they introduce custodial risk. A failure at the exchange level, as seen in past collapses, renders the arbitrage position worthless regardless of the spread. Decentralized protocols mitigate counterparty risk but often suffer from thinner order books, leading to higher slippage when entering or exiting positions.

Operational costs also vary significantly. On-chain strategies require bridging assets, which incurs network fees and time delays. During periods of high network congestion, gas costs can exceed the funding rate income, turning a positive expected return into a net loss. Additionally, the "basis" between the spot price and the perpetual future price must remain stable. If the market moves sharply against your hedge, you may face liquidation risks or significant mark-to-market losses that outweigh the funding payments collected.

Ultimately, the decision rests on your ability to monitor spreads in real-time. Automated bots can capture fleeting opportunities but require robust infrastructure. Manual traders may find better risk-adjusted returns on centralized exchanges with lower complexity, provided they maintain strict capital allocation limits to protect against exchange-specific failures.

Build a decision framework for funding rate arbitrage

Funding rate arbitrage relies on capturing the spread between perpetual futures funding fees across different exchanges. The core mechanism is simple: you hold a long position on an exchange with lower funding rates and a short position on one with higher rates, profiting from the periodic fee payments. However, execution is rarely this clean. The strategy carries distinct risks, including exchange counterparty risk, liquidation cascades, and the cost of capital.

To turn research into a practical plan, you need to evaluate your specific constraints. Are you prioritizing yield stability or raw return? Do you have the infrastructure to manage multiple exchange accounts securely? The following steps outline how to assess these factors and select the right tools for your setup.

Start by determining how much capital you can afford to lock up. Funding arbitrage often requires significant margin to withstand temporary price spikes that trigger liquidations. If you are risk-averse, stick to large-cap assets like BTC or ETH where volatility is lower. If you are comfortable with higher risk, altcoin pairs may offer wider funding spreads but come with greater liquidation danger.

Not all exchanges are created equal. You need platforms that offer deep liquidity for both spot and perpetual markets to minimize slippage. Compare trading fees, withdrawal limits, and, crucially, the reliability of their funding rate calculations. Some smaller exchanges may offer higher rates but suffer from operational issues or poor liquidity, which can trap your capital during critical moments.

Manual tracking is insufficient for this strategy. Use dedicated funding rate scanners and arbitrage tools to identify real-time opportunities. Set up alerts for when the spread exceeds your profit threshold. Additionally, consider using API bots to execute trades instantly, as funding rates can change rapidly. Ensure your monitoring tools provide accurate data on open interest and liquidation levels to avoid unexpected market moves.

Before deploying real capital, run a simulation using historical data. This helps you understand how the strategy would have performed during high-volatility periods. Pay attention to worst-case scenarios, such as simultaneous liquidations on both exchanges. Adjust your position sizes and stop-loss parameters based on these insights to ensure your framework is robust enough to handle market stress.

| Factor | High Yield Focus | Low Risk Focus |

|---|---|---|

| Asset Class | Altcoins with high volatility | Bitcoin or Ethereum |

| Exchange Type | Smaller exchanges with wider spreads | Major centralized exchanges |

| Monitoring | Automated bots required | Manual or semi-automated checks |

| Capital Requirement | Lower margin tolerance | Higher margin for safety |

As an Amazon Associate, we may earn from qualifying purchases.

Watch out for weak options in funding arb

Funding rate arbitrage sounds like free money, but the infrastructure tools often hide the real costs. Many platforms advertise zero-fee transfers, yet ignore the slippage on entry and exit. You are not just trading the spread; you are trading the efficiency of your execution.

The misleading "risk-free" claim

Academic studies on perpetual futures markets show that funding rate arbitrage carries significant tail risk, not zero risk. The strategy involves combining long positions with low funding rates from one exchange with short positions from another with higher funding rates. This works until liquidity dries up or exchange APIs lag. If you assume it is risk-free, you will get rekt during volatile moves.

Weak tools: The hidden fees

Many retail-focused tools do not account for withdrawal fees or network congestion. A tool might show a 5% annualized yield, but after gas fees and trading spreads, your net return could be negative. Always calculate the break-even point including all transaction costs. Do not trust the headline APY.

Comparison of common pitfalls

| Pitfall | Impact | How to spot it |

|---|---|---|

| Ignoring withdrawal fees | Reduces net yield | Check fee schedules for both exchanges |

| API latency | Slippage on entry | Test execution speed during high volatility |

| Exchange counterparty risk | Total loss | Use only regulated or highly audited platforms |

Decision: When to skip

If you cannot monitor positions 24/7, skip this strategy. The margin for error is thin. Use professional-grade infrastructure that offers real-time funding rate tracking and automated rebalancing. Otherwise, you are just gambling with asymmetric risk.

No comments yet. Be the first to share your thoughts!