What is funding rate arbitrage?

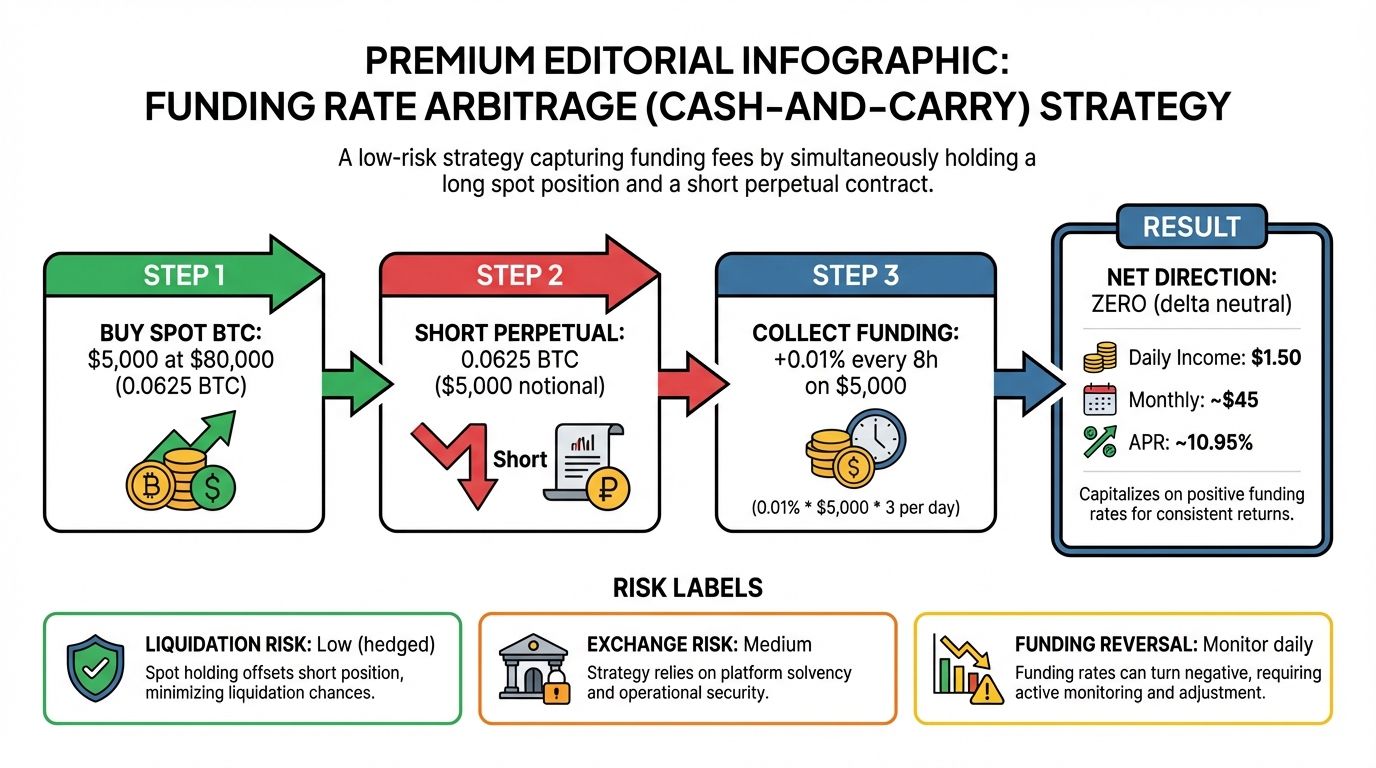

Funding rate arbitrage is a delta-neutral strategy where you simultaneously hold an equal and opposite position in spot and perpetual futures to collect the funding rate while removing directional price exposure. It's also known as a cash-and-carry trade in traditional finance.

The mechanism works on a simple premise: perpetual futures contracts need to stay pegged to the underlying spot price. To achieve this, exchanges charge a "funding rate" every few hours. If the futures price is trading above the spot price (a premium), longs pay shorts. If it's below (a discount), shorts pay longs.

In a typical funding arb setup, you buy the asset on the spot market and short the same amount on the perpetual futures market. This creates a delta-neutral position, meaning you aren't betting on the asset going up or down. Instead, you are collecting the funding payments from the side of the market that is paying out.

For example, if the funding rate is positive, your short futures position receives payments from the long positions. As long as the funding rate remains positive, you earn yield. This strategy is popular among institutional traders and sophisticated retail investors who want to generate consistent returns without exposing their portfolio to market volatility.

Cross-Exchange vs Single-Platform Models

Funding rate arbitrage is a delta-neutral strategy where you simultaneously hold an equal and opposite position in spot and perpetual futures to collect the funding rate while removing directional price exposure [1]. To execute this, you generally choose between two infrastructure approaches: the cross-exchange model or the single-platform model. Each has distinct trade-offs between yield potential and operational risk.

The cross-exchange model involves opening a spot position on one exchange and a short perpetual futures position on another. This approach typically captures the highest yield spreads because it exploits pricing inefficiencies between different venues. However, it introduces significant counterparty risk. You are exposed to withdrawal freezes, exchange insolvency, and the logistical friction of moving assets between platforms. A classic example of this strategy in digital systematic trading is conceptually straightforward but operationally complex [2].

Conversely, the single-platform model executes both the spot and futures legs within the same exchange. This eliminates withdrawal risk and simplifies capital management, as funds remain within a single ecosystem. The trade-off is that yield spreads are often narrower, as internal market efficiency tends to be higher. While the per-trade yield is lower, the reduction in operational overhead and risk can make this model more sustainable for long-term capital deployment.

| Feature | Cross-Exchange Model | Single-Platform Model |

|---|---|---|

| Yield Potential | Higher (exploits inter-exchange spreads) | Lower (internal market efficiency) |

| Counterparty Risk | High (multiple platforms) | Low (single platform) |

| Operational Complexity | High (asset transfers, API management) | Low (internal ledger) |

| Withdrawal Risk | Present | None |

Ultimately, the choice depends on your risk tolerance and operational capacity. Cross-exchange arbitrage offers higher returns but requires robust risk management across multiple venues. Single-platform arbitrage offers stability and simplicity but may require larger capital bases to achieve similar absolute returns.

| Feature | Cross-Exchange | Single-Platform |

|---|---|---|

| Yield Potential | Higher | Lower |

| Counterparty Risk | High | Low |

| Operational Complexity | High | Low |

| Withdrawal Risk | Present | None |

As an Amazon Associate, we may earn from qualifying purchases.

[1] https://www.kraken.com/gr/learn/futures-trading-funding-rate-arbitrage [2] https://www.blockhouse.app/blog/funding-rate-arbitrage

Execution stack and automation

Running a funding rate arbitrage strategy at scale requires moving beyond manual spot-and-futures management. The core infrastructure consists of two layers: a scanner to identify profitable rate differentials and a bot to execute the delta-neutral leg simultaneously across exchanges.

Scanners and bots

Specialized scanners like Arbitrage Scanner aggregate real-time funding rates from multiple venues, allowing you to filter for pairs where the spread exceeds your cost basis. While manual checks are possible for small capital, latency kills margins at scale. Automated bots handle the simultaneous order placement, ensuring your long spot and short perpetual positions open together to lock in the delta-neutral state.

Hummingbot is a prominent open-source framework for this workflow. Its Funding Rate Arbitrage strategy is designed to exploit the differential between funding rates on different exchanges, executing the necessary cross-exchange transfers and order book management automatically. Using a bot reduces the risk of execution lag, which can turn a theoretical profit into a directional loss if the market moves before your hedge is in place.

Live market context

The profitability of these tools depends on the underlying asset's volatility and funding environment. A live look at Bitcoin helps contextualize the baseline conditions for arbitrage opportunities.

Key risks and capital efficiency limits

Funding rate arbitrage is often marketed as a risk-free yield, but that label ignores the structural vulnerabilities inherent in the strategy. While the trade is delta-neutral on paper, real-world execution introduces several failure modes that can erode capital or trigger forced liquidations. Understanding these risks is essential before deploying significant capital.

Exchange Insolvency and Custodial Risk

One of the most severe risks in cross-exchange arbitrage is counterparty failure. When you hold assets on two different platforms—one for the spot position and one for the perpetual futures contract—you are exposed to the solvency of both entities. If one exchange experiences liquidity issues or insolvency, your ability to close positions or withdraw funds may be compromised. This is not merely theoretical; the crypto industry has seen multiple high-profile collapses where user funds were frozen or lost. Holding assets across two platforms effectively doubles your exposure to this specific risk.

Basis Risk and Funding Rate Volatility

The core assumption of funding arb is that the basis (the difference between spot and futures prices) will remain stable or move in a predictable direction. However, basis risk arises when this spread widens unexpectedly or reverses. In highly volatile markets, the funding rate can swing dramatically, turning a previously profitable trade into a losing one. While the strategy is designed to hedge directional price movement, it does not hedge against changes in the cost of carry. If the funding rate turns negative or drops significantly, the income stream that sustains the trade can vanish or reverse, leading to losses even if the underlying asset price remains stable.

Liquidation Cascades and Margin Calls

Even with careful margin management, liquidation cascades pose a significant threat. Perpetual futures contracts require maintenance margin, and a sudden adverse price movement can trigger a margin call. If the market moves against your futures position faster than you can rebalance your spot hedge, you may face liquidation. This is particularly dangerous during periods of high volatility or low liquidity, where slippage can exacerbate losses. A liquidation cascade occurs when one trader's forced liquidation triggers a chain reaction, causing further price movements that liquidate other positions. This systemic risk can wipe out capital quickly, regardless of the strategy's theoretical neutrality.

Capital efficiency limits to account for

Finally, the capital efficiency of funding arb is often overstated. To achieve meaningful returns, traders must deploy significant capital due to the relatively small size of funding payments. This large capital requirement ties up funds that could be deployed elsewhere, reducing overall portfolio efficiency. Additionally, the need to maintain margin on both sides of the trade means that a substantial portion of capital is locked as collateral, further limiting flexibility. Traders must carefully calculate the net return after accounting for fees, margin requirements, and potential slippage to ensure the strategy remains viable.

Pre-deployment checklist for funding arb strategy

Before moving capital, you must verify that every component of your delta-neutral setup can execute without friction. Funding rate arbitrage relies on precise timing and low latency; a single broken link in your operational chain can turn a theoretical profit into a realized loss.

Ensure your API keys have trading and withdrawal permissions enabled on both exchanges. Check that your daily withdrawal limits are set high enough to cover potential rebalancing needs or margin calls without requiring manual intervention.

Different exchanges calculate and pay funding rates at different intervals (e.g., every 8 hours vs. every 4 hours). Align your positions so that you are long spot and short futures at the exact moment of payment. Misalignment here is the most common source of lost yield.

Execute a small test transfer between the two exchanges. Verify that the network confirms transactions quickly enough to allow you to rebalance your delta if the spot-futures basis diverges significantly. Slow networks can trap your capital during volatile periods.

Calculate the net funding rate after subtracting trading fees, withdrawal fees, and deposit fees. The spread must consistently exceed these costs. If the net rate is razor-thin, a small price movement or fee change can erase your edge.

Once these checks are complete, you can deploy with confidence. Remember that this strategy requires ongoing maintenance, not just a one-time setup.

Funding arbitrage strategy: common: what to check next

Funding rate arbitrage is a delta-neutral strategy where you simultaneously hold an equal and opposite position in spot and perpetual futures to collect the funding rate while removing directional price exposure [1]. It's also known as a cash-and-carry trade in traditional finance.

For example, a stock trading at $50 on the New York Stock Exchange (NYSE) and $50.10 on the London Stock Exchange (LSE) presents an arbitrage opportunity. Arbitrageurs can buy the stock on the NYSE at the lower price and sell it on the LSE at the higher price, capturing the $0.10 price difference per share [2].

No comments yet. Be the first to share your thoughts!