How funding rate arbitrage works

Funding rate arbitrage is a market-neutral strategy designed to capture the periodic interest payments exchanged between traders in the perpetual futures market. The core mechanism is simple: you hold a long position in the spot market while simultaneously holding a short position in the perpetual futures contract for the same asset. Because these positions are equal in size but opposite in direction, price movements in the underlying asset largely cancel each other out, isolating the funding fee as the primary source of return.

To understand why this fee exists, it helps to look at how perpetual contracts differ from traditional futures. Traditional futures have an expiration date, which forces the contract price to converge with the spot price at delivery. Perpetual contracts have no expiration, so they need a different mechanism to keep the contract price anchored to the spot price. That mechanism is the funding rate.

The funding rate is a periodic payment exchanged between long and short traders, typically every eight hours. When the market is bullish and the perpetual price trades at a premium to the spot price, longs pay shorts. This payment incentivizes traders to open short positions, which pushes the futures price down toward the spot price. Conversely, when the market is bearish and the perpetual price trades at a discount, shorts pay longs. This encourages new long positions, pulling the futures price back up.

In a funding rate arbitrage setup, you are the short side of the perpetual contract. By holding a hedged position, you collect these payments from the longs whenever the market is in a state of contango (futures premium). This structure allows you to generate yield from the market's natural leverage bias without taking on directional price risk. The profitability depends on the spread between the funding rate received and the costs of borrowing or trading, making it a staple for quantitative funds and institutional traders seeking stable income in volatile markets.

New infrastructure changes the math

Funding rate arbitrage has shifted from a theoretical concept to a structural market feature. The 2026 landscape is defined by new decentralized exchanges (DEXs), improved oracle latency, and faster cross-chain bridges. These changes directly impact execution speed and cost, moving the strategy beyond basic theory into a realm of precise, infrastructure-dependent execution.

The core mechanic remains the same: capturing the spread between spot and perpetual funding rates. However, the infrastructure now allows for near-instantaneous rebalancing. New DEXs offer deeper liquidity pools with tighter spreads, reducing the slippage that previously ate into profits. Improved oracle latency ensures that price feeds are more accurate, minimizing the risk of unfavorable mark price updates during volatile periods.

Cross-chain bridges have also evolved. What once took minutes now happens in seconds, allowing arbitrageurs to move capital between chains with minimal delay. This speed is critical. Funding rates can change rapidly, and the ability to act quickly on these changes is what separates profitable strategies from stagnant ones. The infrastructure now supports a more dynamic and responsive approach to arbitrage.

The result is a market where opportunities are more frequent but require more sophisticated execution. Traders must leverage these new tools to stay competitive. The infrastructure changes have lowered the barrier to entry but raised the bar for execution quality. Success now depends on how well you can integrate these new technologies into your strategy.

Cross-exchange vs same-exchange flows

Funding rate arbitrage generally falls into two distinct buckets: cross-exchange arbitrage and same-exchange cash-and-carry. The choice between them dictates your risk profile, capital efficiency, and operational complexity. Cross-exchange strategies chase wider spreads but introduce significant counterparty and transfer risks. Same-exchange approaches prioritize stability and speed, accepting narrower margins in exchange for reduced friction.

Cross-exchange arbitrage

Cross-exchange funding arbitrage involves opening offsetting positions on two different platforms. You typically go long on an exchange with a low or negative funding rate and short on an exchange with a high positive rate. The goal is to capture the difference between the two rates while the spot price movements offset each other across the two venues.

This method often offers higher potential yields because fragmented liquidity can create wider discrepancies between exchanges. However, the risks are substantial. You must manage deposits, withdrawals, and transfer times, which exposes you to network congestion and exchange delays. If a withdrawal is stuck during a volatile market move, your hedge may break, leaving you fully exposed to price risk. Additionally, you face counterparty risk on both platforms; if one exchange halts withdrawals or experiences an outage, your capital is trapped.

Same-exchange cash-and-carry

Same-exchange arbitrage, often called cash-and-carry, executes both legs of the trade on a single platform. You buy the underlying asset in the spot market and simultaneously sell a perpetual futures contract. This structure eliminates transfer risk and withdrawal delays since both positions reside in the same account.

The primary advantage is operational simplicity and speed. You can open and close the hedge instantly, reacting quickly to changes in funding rates. The downside is that spreads are generally tighter. Because most major liquidity pools converge on the same few centralized exchanges, the difference between the spot price and the perpetual futures price is usually smaller. You are trading higher frequency, lower-margin opportunities for lower operational overhead and reduced counterparty exposure.

Strategy comparison

The table below summarizes the structural differences between these two execution methods. Use this to determine which approach aligns with your risk tolerance and technical capabilities.

| Feature | Cross-Exchange | Same-Exchange |

|---|---|---|

| Spread Potential | Higher | Lower |

| Transfer Risk | High | None |

| Counterparty Risk | Two platforms | One platform |

| Execution Speed | Slower | Instant |

| Complexity | High | Low |

The Hidden Risks of Funding Arbitrage

Funding rate arbitrage is often marketed as a risk-free income stream, but this characterization ignores the mechanical realities of high-leverage trading. While the strategy aims to capture the spread between spot and perpetual futures, it exposes capital to three distinct failure modes: liquidation cascades, exchange solvency failures, and smart contract vulnerabilities. Understanding these risks is essential for any trader treating this as a core infrastructure component rather than a speculative bet.

Liquidation Cascades

The most immediate threat to funding arbitrage positions is the liquidation cascade. Even when a position is hedged, a sharp move in the underlying asset price can trigger margin calls on one side of the trade. If the exchange’s liquidation engine is slow or the market is illiquid, the position may be closed at a significant loss, leaving the arbitrageur with an unhedged exposure. This is particularly dangerous during high-volatility events, such as major macroeconomic announcements or regulatory news, when funding rates can diverge sharply from spot prices.

Exchange Solvency

Counterparty risk remains a critical concern in crypto arbitrage. Unlike traditional finance, where clearinghouses often guarantee trades, crypto exchanges operate as opaque entities. If an exchange faces liquidity issues or insolvency, funds deposited for margin can be frozen or lost entirely. This risk is exacerbated in decentralized finance (DeFi), where smart contracts may be exploited or drained. Traders must constantly monitor exchange health indicators, including on-chain reserves and withdrawal status, to mitigate this exposure.

Smart Contract Vulnerabilities

For DeFi-based funding arbitrage, smart contract code is the final line of defense. Bugs in lending protocols or perpetual exchange contracts can lead to total loss of capital. Even if the arbitrage logic is sound, a vulnerability in the underlying protocol can be exploited by attackers. Regular audits and bug bounty programs are standard, but they are not foolproof. Traders should diversify across multiple protocols and avoid concentrating large amounts of capital in a single contract.

Funding arb execution checklist

A funding arb position requires simultaneous, offsetting trades to isolate the funding rate. Without strict synchronization, you expose yourself to directional risk rather than capturing the spread. This checklist walks you through the setup, ensuring you verify data, execute legs, and monitor for liquidation.

Before entering, confirm the current funding rate on both exchanges. Rates change every 8 hours on major platforms like Binance and Hyperliquid. Use a reliable data provider to see the exact rate for your entry time. Do not rely on cached data from previous intervals.

Subtract trading fees, withdrawal costs, and potential slippage from the gross funding rate. A spread that looks profitable on paper may turn negative once you account for the maker/taker fees on both legs. Ensure the net yield exceeds your cost of capital.

Open the spot position and the perpetual futures position simultaneously. Use identical asset amounts to ensure delta neutrality. If one leg executes significantly before the other, you are exposed to market movement. Use limit orders to control entry prices.

Although the position is market-neutral, exchange liquidation can occur if one side moves drastically against your margin. Set tight stop-losses or alerts for margin ratio thresholds. Monitor the funding rate trend; if it flips against your position, the trade thesis may no longer hold.

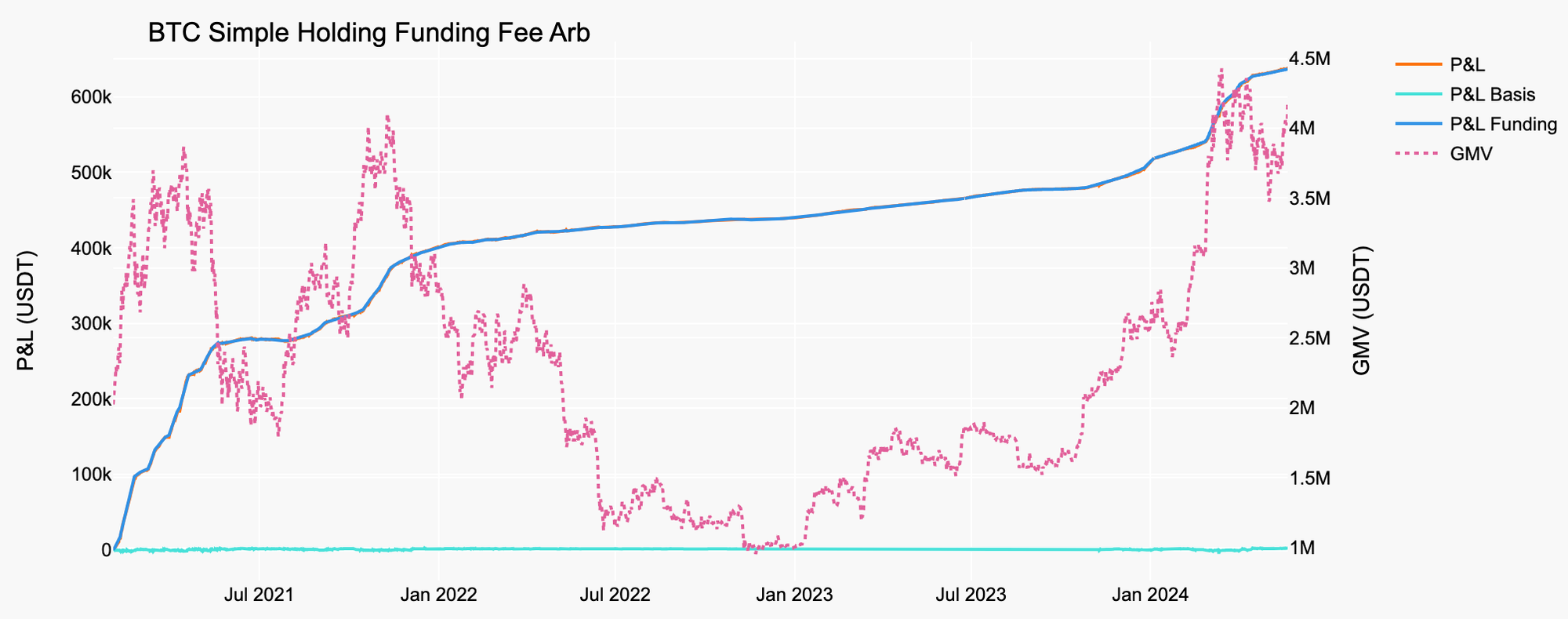

The chart above shows the underlying asset price action. While your funding arb is neutral to this price movement, extreme volatility can trigger liquidation if margin is insufficient. Keep a buffer above the maintenance margin requirement.

Common questions about funding arb

Funding arbitrage is a straightforward concept: borrow capital at a low interest rate and invest it where it generates higher returns. In practice, this involves combining long positions on exchanges with low funding rates against short positions on exchanges with higher rates. While the mechanics are simple, the execution requires precise timing and risk management.

How to do funding rate arbitrage?

Classic cross-exchange arbitrage requires simultaneous execution. You open a long position on a spot exchange while opening a short position on a perpetual contract on another exchange. The goal is to capture the difference in funding payments. For example, if you receive funding on the long side but pay less on the short side, the spread becomes your profit. This strategy relies on maintaining equal quantities and offsetting price risks.

Is funding rate arbitrage profitable?

Funding arbitrage can provide stable income, but it is not risk-free. Profits are typically small per trade—often 0.1% to 0.5% spreads in liquid markets—but they are scalable. However, extreme price spikes can trigger liquidation on one side of the position. If the market moves sharply against your hedge, you may face margin calls even if the funding payments remain positive. Risk management is essential to protect capital.

What is a funded arbitrage?

Perpetual contract funding rate arbitrage refers to the simultaneous execution of two transactions in the spot and perpetual contract markets. These positions involve the same underlying asset, opposite directions, and equal quantities. The profits and losses from price movements offset each other, leaving the funding rate differential as the primary source of return. This structure is designed to be market-neutral, isolating the yield from funding payments.

No comments yet. Be the first to share your thoughts!