Funding arb limits to account for

Funding Arb Strategy works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Funding arb choices that change the plan

Funding rate arbitrage is not a passive income machine; it is a mechanical tradeoff between yield and exposure. To evaluate whether the strategy fits your 2026 infrastructure, you must weigh three concrete factors: capital efficiency, execution friction, and market regime risk.

Capital Efficiency and Leverage

The primary allure of funding arb is the ability to capture yield without directional exposure. However, this requires significant capital to absorb the spread between borrowing costs and futures yield. Unlike spot trading, you must maintain margin on both legs of the trade. If you use leverage, a sudden price spike can liquidate your spot position while your short futures remain open, creating a "gap risk" scenario where the hedge fails. The tradeoff here is simple: higher leverage increases potential ROI but exposes you to binary liquidation events.

Execution Friction and Slippage

Funding rates settle periodically (often every 8 hours), but price movements are continuous. The difference between the funding rate you expect and the entry/exit price you actually get can erode profits. On high-volume pairs like BTC or ETH, slippage is minimal. On lower-cap altcoins, the spread between the bid and ask can exceed the funding yield itself, turning a theoretical profit into a loss. You must factor in trading fees for both the spot purchase and the futures short. If your exchange offers fee rebates for market makers, this tradeoff shifts in your favor; otherwise, it becomes a friction-heavy operation.

Market Regime Risk

Funding rates are mean-reverting but can stay skewed for weeks during extreme bull or bear markets. A positive funding rate (longs pay shorts) is common in rallies. If the market cools abruptly, the funding rate can flip negative, turning your "risk-free" short leg into a paying leg. This is not a bug; it is a feature of the market. The tradeoff is that you are betting on the persistence of market sentiment. If you are wrong about the regime, you pay for the privilege.

| Factor | Risk | Mitigation |

|---|---|---|

| Liquidation | Price spike wipes spot margin | Maintain low leverage (<2x) |

| Slippage | Entry/exit costs exceed yield | Trade only high-volume pairs |

| Regime Flip | Funding rate turns negative | Monitor open interest trends |

The data above shows how price action and volume interact. In funding arb, you are not betting on the direction of this chart. You are betting on the divergence between the spot price and the futures price. When that divergence widens, funding rates spike. When it narrows, they compress. Your edge lies in identifying these divergences before they normalize.

Build a Funding Arb Strategy 2026 Decision Framework

Funding rate arbitrage relies on capturing the spread between perpetual swap rates and spot prices. In 2026, the strategy demands more than just finding a positive rate; it requires a disciplined checklist to ensure the spread survives trading fees, slippage, and exchange risk. Without a structured approach, the theoretical profit often vanishes against execution costs.

Use the following steps to evaluate and execute a trade. Each step represents a critical filter in your decision framework.

The gross spread must exceed the sum of maker/taker fees on both legs. Calculate the annualized yield, then subtract the cost of opening and closing the position. If the net yield is less than 5-10% after fees, the trade is rarely worth the capital lock-up.

Funding arb requires holding positions on two different platforms. If one exchange freezes withdrawals or experiences an outage, you are exposed to directional market risk. Stick to Tier-1 exchanges with proven liquidity and transparent proof-of-reserves to mitigate this specific risk.

Look at the 7-day average funding rate, not just the current 8-hour snapshot. Rates can spike temporarily due to short-term liquidations. If the historical average is near zero, the current spike is likely a transient anomaly that will revert before you collect significant yield.

Use a calculator to model the trade over your intended holding period. Include slippage on entry and exit. For example, if you are long spot and short perp, ensure the basis converges as expected. A widening basis can cause unrealized losses that exceed your funding gains if you are forced to close early.

As an Amazon Associate, we may earn from qualifying purchases.

Final Checklist for Execution

Before deploying capital, run through this quick verification list:

-

Net yield > 10% after all fees and estimated slippage

-

Both exchanges are Tier-1 with high liquidity

-

7-day average funding rate is positive and stable

-

Basis convergence risk is assessed for your holding period

-

Withdrawal limits and transfer times are confirmed

Funding rate arbitrage is profitable when executed with precision. It is not a passive income stream but an active trading strategy that requires constant monitoring and risk management.

Watchouts in Funding Rate Arbitrage

The promise of risk-free yield from funding rate arbitrage often masks structural risks that can erode capital. Traders frequently overlook the mechanical and market-specific flaws that turn theoretical spreads into real losses. Before deploying capital, you must identify which components of the strategy are fragile.

Misleading Annualized Yield Claims

Many calculators project annualized returns based on current funding rates without accounting for rate volatility. A 0.05% rate every eight hours looks like 14% annually, but funding rates are mean-reverting and often collapse during low-volatility periods. Basing position sizing on peak rates rather than median historical averages leads to over-leveraged positions when the spread narrows.

Exchange Counterparty and Latency Risk

Arbitrage relies on simultaneous execution across exchanges. If one exchange delays settlement or experiences a withdrawal halt, your hedge breaks. Hyperliquid and Binance operate on different matching engines and settlement times. A latency spike of even a few seconds can turn a positive spread into a negative one as prices diverge. Always verify withdrawal limits and network congestion before entering.

Hidden Funding Rate Mechanics

Not all exchanges calculate funding the same way. Some use simple time-weighted averages, while others incorporate volatility adjustments or liquidation cascades. A rate that appears favorable on one platform may be artificially suppressed or inflated by market makers manipulating the order book. Check the funding calculation formula for each exchange to ensure you are comparing like with like.

Liquidation Cascades in Volatile Markets

During high volatility, funding rates can spike dramatically, signaling extreme sentiment. While this offers higher yield, it also increases the risk of liquidation if prices move against your spot or futures position. The spread may widen, but the cost of maintaining the hedge through a sharp move can exceed the funding income. Stress-test your positions against 5-10% adverse price movements.

Regulatory and Compliance Blind Spots

Cross-exchange arbitrage may trigger regulatory scrutiny if not structured correctly. Some jurisdictions view automated funding rate harvesting as market manipulation if it involves wash trading or layering. Ensure your strategy complies with local financial regulations and exchange terms of service to avoid account freezes or legal action.

Funding rate arbitrage: practical questions and choices that change the plan

Before deploying capital into delta-neutral strategies, it is essential to understand the mechanics and realistic return profiles. Funding rate arbitrage is not a passive income guarantee; it is a tactical trade that requires active management of basis risk and exchange reliability.

How to execute funding rate arbitrage?

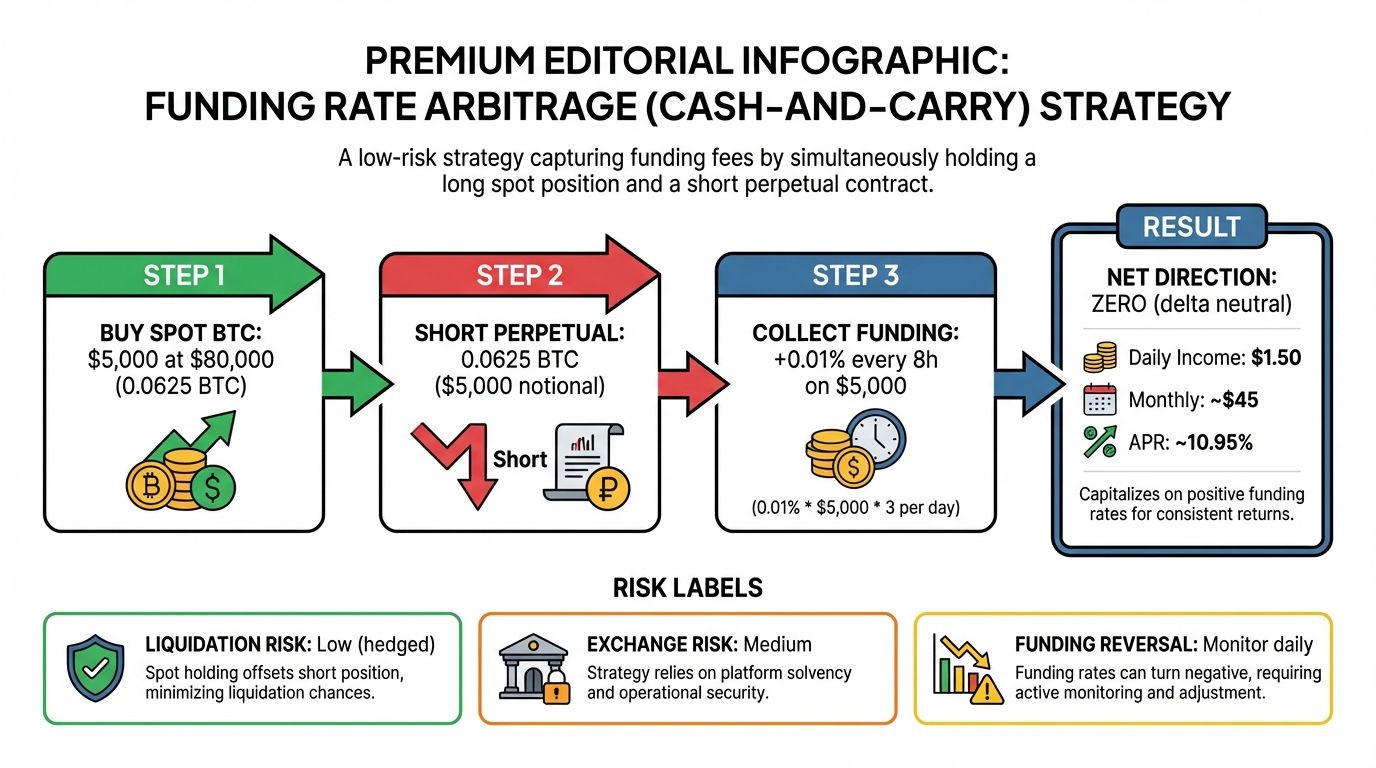

The core mechanism involves taking opposite positions on two venues to capture the funding rate differential. For example, if Binance pays a positive funding rate while Hyperliquid charges one, you would go long on Binance and short Hyperliquid. You receive the spread between the two rates every eight hours. This structure isolates the funding cash flow from directional market moves, assuming the spread remains stable or moves in your favor.

Is funding rate arbitrage profitable in 2026?

Profitability depends entirely on the net basis after fees. While some strategies target 8-20% APY during high volatility, these returns are not consistent. Negative funding periods can erode capital, and exchange fees often cut into the gross spread. You must calculate the net yield by subtracting trading fees, withdrawal costs, and potential slippage from the gross funding differential to determine if the trade justifies the risk.

What are the main risks of this strategy?

The primary risk is spread convergence or reversal. If the funding differential narrows or flips, your hedge may no longer offset the cost of carry. Additionally, exchange-specific risks exist, such as withdrawal halts or liquidity crunches during extreme market conditions. Counterparty risk is also a factor; if an exchange freezes funds or experiences an outage, your delta-neutral position can become exposed to directional losses.

How often do funding rates reset?

Most major centralized exchanges reset funding rates every eight hours, typically at 00:00, 08:00, and 16:00 UTC. This frequency means you are exposed to funding calculations three times daily. Some decentralized perpetual protocols may have different intervals, such as every hour or every block, which can increase the complexity of tracking and managing your positions across multiple venues.

No comments yet. Be the first to share your thoughts!