Funding arb strategy limits to account for

Use this section to make the Funding Arb Strategy decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Funding arb strategy choices that change the plan

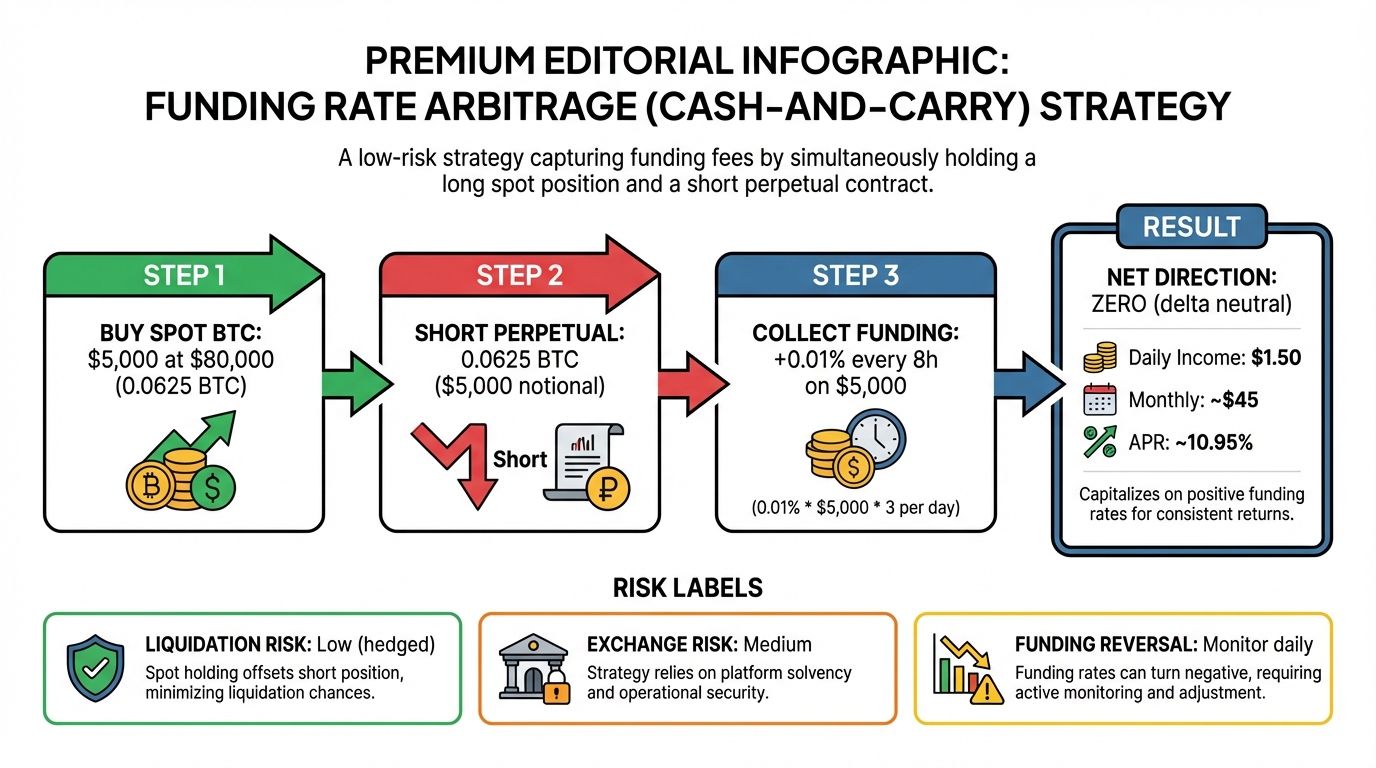

Funding rate arbitrage aims to collect periodic payments from crypto perpetual futures markets without taking on directional price risk. The core mechanic is simple: hold a long spot position and a short perpetual futures position of equal value. When the funding rate is positive, shorts pay longs. When negative, longs pay shorts. In theory, price movements cancel out, leaving the funding rate as your primary profit source.

However, the strategy is not risk-free. Several concrete factors can erode or eliminate your expected yield. Understanding these tradeoffs is essential before deploying capital.

Liquidity and Slippage

The most immediate friction point is execution cost. Funding arb requires entering two positions simultaneously. If you lack sufficient liquidity on either the spot or futures market, slippage can eat into your basis. This is especially true for smaller-cap assets where order books are thinner. If the spread between the spot price and the perpetual futures price is narrow, the cost to enter the trade may exceed the expected funding yield over the holding period. Always calculate the net basis after fees before assuming a profitable setup.

Exchange Counterparty Risk

By holding assets on two different venues, you double your exposure to exchange solvency and operational risk. If one exchange halts withdrawals or experiences a technical outage during a volatile market move, you may be unable to rebalance or exit the hedge. This is particularly relevant in cross-exchange funding arbitrage, where you might be long on Exchange A and short on Exchange B. A failure on one side leaves you with an unhedged directional exposure. Diversifying across reputable, regulated platforms mitigates this, but it does not eliminate it.

Capital Efficiency and Opportunity Cost

Funding arb is capital-intensive. You must post margin for both the spot purchase and the futures position. While the futures position is hedged, exchanges still require initial and maintenance margin. This ties up significant capital that could otherwise be deployed in higher-yield or more liquid opportunities. Additionally, funding rates are not static. They fluctuate based on market sentiment, often spiking during bull markets and turning negative during bear markets. Periods of low or negative funding rates can result in zero or negative yield, making the strategy inefficient during certain market cycles.

Comparison of Funding Arb Models

Different variations of the strategy present distinct risk and return profiles. The table below compares the most common approaches.

| Model | Primary Risk | Typical Yield Source | Operational Complexity |

|---|---|---|---|

| Cross-Exchange | Counterparty & Withdrawal | Rate differential between exchanges | High |

| Single-Exchange Spot/Futures | Exchange Solvency | Positive funding rates | Low |

| Index Arbitrage | Index calculation lag | Basis convergence | Medium |

When It Makes Sense

Funding rate arbitrage is most effective in markets with consistent, positive funding rates and deep liquidity. It suits traders who prioritize capital preservation over aggressive growth and have the infrastructure to manage multi-exchange operations. It is less suitable for those seeking high returns or those uncomfortable with the operational overhead of managing hedged positions across multiple platforms. Before entering, verify the current basis, assess the liquidity depth of both legs, and ensure your exchange accounts are fully compliant and secure. The yield is real, but it is not free; it is compensation for the operational and counterparty risks you assume.

How to choose the right funding arb approach

Funding rate arbitrage is a way to collect funding payments from the crypto futures market without taking on directional price risk. You hold equal and opposite positions in spot and perpetual futures, so price movements cancel out and the funding rate becomes your profit and loss. However, the strategy is not a simple set-it-and-forget-it system. Infrastructure shifts in 2026 have changed how exchanges calculate and settle these fees, making tool selection and risk management more critical than ever.

To navigate this, you need a practical decision framework. The right approach depends on your capital size, technical capabilities, and risk tolerance. Below is a step-by-step guide to building your strategy.

Small accounts (under $10,000) often struggle with exchange fees eating into thin margins. Medium accounts ($10,000–$100,000) have flexibility to spread capital across two or three exchanges to capture rate differentials. Large accounts ($100,000+) can access institutional-grade tools and negotiate fee rebates, making cross-exchange arbitrage highly efficient.

Manual execution is low-cost but slow, suitable for those monitoring rates a few times a week. Automated bots handle the speed needed to catch transient rate spikes but require coding knowledge or subscription fees. Hybrid approaches use alerts for manual entry during high-volatility events, balancing control and efficiency.

Not all exchanges treat funding payments equally. Some have changed settlement times or introduced new fee structures. Always check the exchange’s official documentation for current funding intervals (8-hour, 4-hour, or hourly) and any minimum position requirements. Avoid platforms with poor liquidity, as slippage can erase your arbitrage edge.

Funding rates are dynamic. A positive rate today might turn negative tomorrow if market sentiment shifts. Regularly rebalance your spot and futures positions to maintain a delta-neutral stance. Use price widgets to track the underlying asset’s performance and ensure your hedge remains effective.

| Method | Cost | Speed | Best For | Best For |

|---|---|---|---|---|

| Manual | Low | Slow | Beginners | Beginners |

| Bot | High | Fast | Pro traders | Pro traders |

| Hybrid | Medium | Medium | Intermediate | Intermediate |

The choice between manual, automated, and hybrid methods ultimately comes down to your resources. Manual trading offers control but lacks the speed to capitalize on fleeting opportunities. Bots provide efficiency but introduce technical risk and ongoing costs. Hybrid strategies offer a middle ground, allowing you to intervene when conditions are most favorable.

Watchouts in funding arbitrage

Funding rate arbitrage collects payments from the crypto futures market without directional price risk. You hold equal and opposite positions in spot and perpetual futures, so price movements cancel out and the funding rate becomes your P&L [src-serp-2]. The strategy can be profitable, but only if you account for hidden costs and execution risks [src-serp-1].

Many traders overestimate returns by ignoring slippage and fees. A small spread between exchanges can erase your margin. Always calculate net yield after trading fees, withdrawal costs, and potential liquidation risks.

Use a live chart to monitor funding rate trends and volatility before entering positions.

Funding arbitrage: what to check next

Funding rate arbitrage is a market-neutral strategy where traders hold equal and opposite positions in spot and perpetual futures markets. By capturing the periodic funding payments exchanged between long and short traders, the strategy generates yield independent of asset price direction.

The following answers address the most common practical objections and clarifications regarding this approach in the current market infrastructure.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!