How funding rates create arb opportunities

Perpetual swaps don't expire. They are designed to track the spot price of the underlying asset indefinitely. To keep the perpetual price anchored to the spot price, exchanges use a mechanism called the funding rate. This is a periodic payment exchanged between traders holding long positions and those holding short positions.

The system works on a simple principle: if the perpetual price trades higher than the spot price (a premium), longs pay shorts. If the perpetual trades lower (a discount), shorts pay longs. These payments typically occur every eight hours. The rate adjusts dynamically based on market sentiment and demand, creating a direct cash flow stream independent of the asset's price direction.

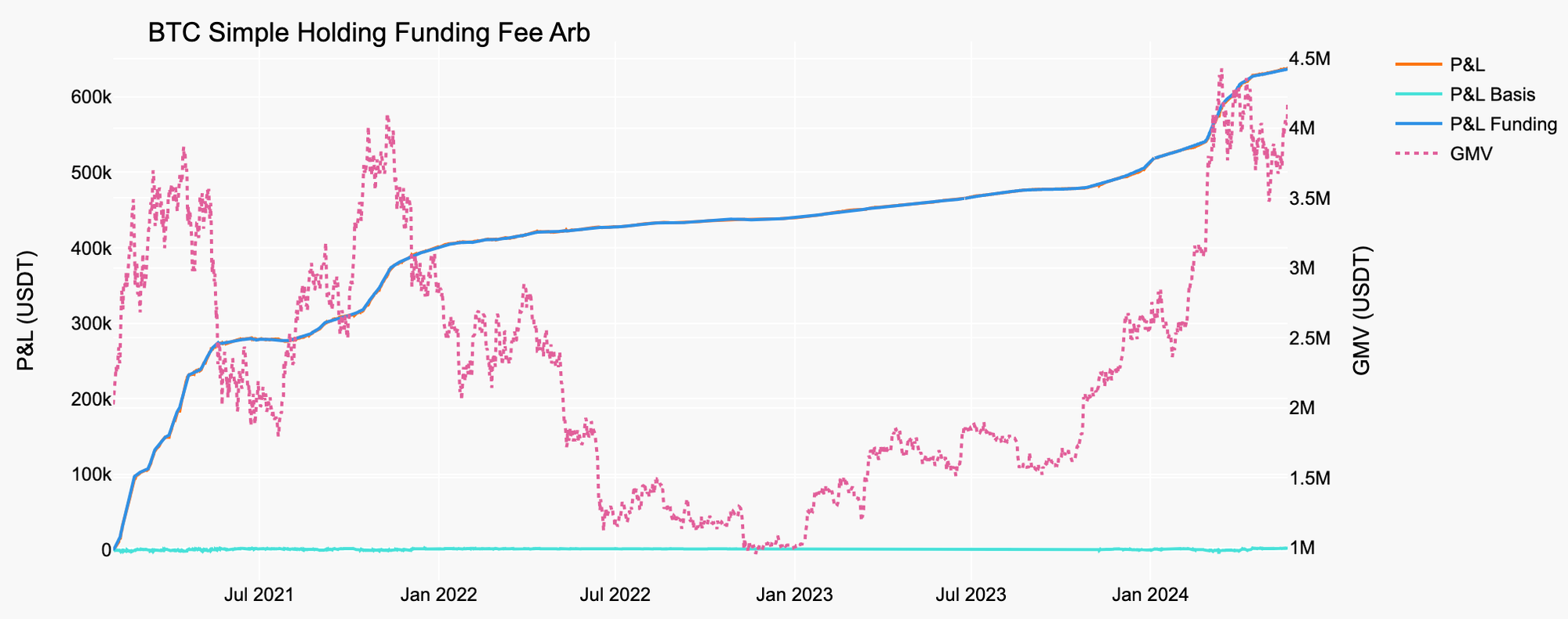

Funding arbitrage exploits the spread between these rates. A trader can hold a long position on one exchange where they receive funding while simultaneously holding a delta-neutral short position on another exchange where they pay funding. If the funding received exceeds the funding paid, the position generates profit from the rate differential rather than market movement.

This spread is distinct from the basis—the difference between the perpetual and spot prices. While the basis converges to zero as prices align, the funding rate fluctuates with trader sentiment. In bull markets, longs are eager to leverage up, pushing rates higher. This creates a tradable opportunity for those willing to provide the counter-party liquidity through delta-neutral hedging.

How spot-futures hedging works

Spot-futures hedging is the mechanical foundation of delta-neutral funding rate arbitrage. The goal is simple: hold a long position in the underlying asset while holding an equal short position in the corresponding perpetual futures contract. Because the two positions move in opposite directions, price fluctuations cancel each other out, leaving you with zero delta (price exposure). Your profit, or loss, depends entirely on the funding rate paid between the two legs.

To execute this, you need to understand the relationship between the spot price and the futures price. In a healthy market with positive funding rates, the perpetual futures price trades at a premium to the spot price (contango). This premium exists because traders are willing to pay a fee to maintain their long leveraged positions. By shorting the futures, you collect this fee from the longs every time the funding interval hits—typically every eight hours.

The mechanics rely on a 1:1 ratio. If you buy $10,000 worth of Bitcoin on spot, you must open a $10,000 notional short position in the BTC perpetual futures. This ensures that if Bitcoin drops 10%, your spot position loses $1,000, but your short futures position gains $1,000. The net PnL from price movement is zero. You are not betting on Bitcoin going up or down; you are betting that the funding payments will exceed your trading fees and liquidation risks.

Scan perpetual markets for assets with consistently positive funding rates. You want a market where longs are paying shorts, indicating bullish sentiment and leverage. Avoid assets with negative or near-zero rates, as there is no yield to capture. Look for rates that have remained positive over several intervals, not just a single spike.

Purchase the underlying cryptocurrency on a spot exchange. This establishes your delta-neutral base. Ensure you have enough capital to cover both the spot purchase and the margin required for the futures hedge. Spot liquidity should be deep enough to allow for immediate execution without significant slippage.

Simultaneously open a short position in the perpetual futures contract with the same notional value as your spot holding. Use isolated margin to limit risk to the futures leg only. This step locks in the delta-neutral state. If your spot holding is $10,000, your short futures position must also be $10,000 notional.

Even though your portfolio is delta-neutral, your futures position is leveraged and can be liquidated if the market moves sharply against you. Monitor your maintenance margin levels closely. If the price rallies hard, your short futures position will incur losses that require additional margin to prevent liquidation, which would break your hedge.

Cross-exchange rate differentials

Funding rates are not uniform across the crypto ecosystem. They fluctuate based on local supply and demand for leverage on each platform. A rate of +0.1% on Binance might sit at +0.05% on Bybit, or even drop to negative on a decentralized exchange like Hyperliquid. These discrepancies create the core opportunity for cross-exchange arbitrage.

The strategy relies on executing a delta-neutral position across two venues. You go long perpetuals on the exchange with the higher funding rate (receiving the payment) and short perpetuals on the exchange with the lower rate (paying the payment). The goal is to capture the spread while hedging directional risk. If executed correctly, your PnL from price movement nets out, leaving the funding differential as your profit source.

However, the spread is rarely risk-free. It must exceed the combined costs of trading fees, withdrawal fees, and the friction of moving capital between exchanges. Liquidity depth also varies. A favorable rate on a smaller exchange might be trapped behind thin order books, making entry and exit costly or impossible at scale.

The table below illustrates how these differentials manifest in real market conditions. Note how the funding cost for the same asset can diverge significantly depending on the venue's liquidity and user sentiment.

| Exchange | BTC Funding (8h) | ETH Funding (8h) | BTC Withdrawal Fee |

|---|---|---|---|

| Binance | +0.04% | +0.03% | 0.0005 BTC |

| Hyperliquid | -0.01% | +0.02% | N/A (On-chain) |

| Bybit | +0.03% | +0.02% | 0.0004 BTC |

| OKX | +0.05% | +0.04% | 0.0005 BTC |

When analyzing these spreads, always account for the timing of payments. Most centralized exchanges pay every 8 hours, while decentralized platforms may have different intervals. Misaligning these schedules can introduce unexpected cash flow gaps that erode your net yield. Always verify the exact payment frequency and settlement time on each platform before executing the trade.

Calculate net APY and fees

Spotting a high funding rate is only half the battle. If you ignore the friction costs, your "profitable" trade might actually be a loss. To execute delta-neutral crypto trades correctly, you need to strip away the noise and look at the true net yield.

Think of the funding rate as your gross revenue. It’s the raw interest you collect every 8 hours (or whatever interval the exchange uses). But exchanges don’t trade for free. You pay taker fees when you open and close positions, and you often pay maker fees on the spot side. Then there’s slippage—the price difference between your order and the actual fill. These costs eat directly into your basis.

Here is the concrete framework for your calculation:

Net APY = (Gross Funding Income - Trading Fees - Slippage) × (365 / Funding Intervals)

Let’s break it down with a realistic example. Suppose you see an 8-hour funding rate of 0.05% on Binance. That sounds like 18.25% APY on paper. But if you pay 0.04% in taker fees to enter and 0.04% to exit, your cost is 0.08% per cycle. Your net gain per 8 hours is only 0.05% - 0.08% = -0.03%. You’re losing money on every interval.

Slippage adds another layer of risk. If you’re trading a volatile asset like BTC, the price might move against you while your order is filling. Always assume a small slippage buffer (e.g., 0.01-0.02%) in your model. If the net APY after all deductions is less than 5-10%, the risk of liquidation or exchange downtime may not be worth it. Use a

to monitor current market conditions and adjust your entry points accordingly.Finally, keep an eye on the

to gauge market volatility. High volatility often correlates with higher funding rates, but also higher slippage. Balance the two carefully.Managing liquidation and counterparty risk

Delta-neutral doesn't mean risk-free. You are still exposed to the mechanics of how the trade is built. The primary dangers are exchange insolvency, smart contract failures, and the specific risk of liquidation when the basis diverges unexpectedly.

Diversify custody to avoid single-point failure

Never hold your entire portfolio on one exchange. If that platform halts withdrawals or becomes insolvent, your delta-neutral position can turn into a total loss. Spread your spot holdings and futures margins across at least two reputable, regulated venues. This is your first line of defense against counterparty risk.

Watch the basis, not just the funding rate

Liquidation events in funding arbitrage rarely happen because the funding rate stops. They happen because the basis (the difference between spot and futures price) moves against your hedge. If the futures price spikes significantly higher than spot, you may face margin calls on your short futures leg even if your spot asset is stable. Monitor the basis spread closely; a widening basis can erode your margin buffer faster than you expect.

Audit smart contract exposure

If you are using decentralized exchanges (DEXs) or lending protocols for your arbitrage, you are exposed to smart contract bugs. Unlike centralized exchanges, there is no customer support to reverse a hack. Stick to audited, time-tested protocols and keep position sizes within your comfort zone. Understand that "neutral" only protects you from directional market risk, not execution or platform risk.

Funding rate arbitrage in 2026

The landscape for delta-neutral crypto trades has shifted dramatically as institutional adoption matures. In 2026, the entry of large-scale capital through spot ETFs and traditional finance infrastructure has normalized funding rate volatility, making the "easy" spreads less persistent than in previous bull markets. This maturation means that alpha now comes from speed and structural nuance rather than simple spread hunting.

Institutional flows have altered the basis dynamics. While retail-driven spikes still occur, the sheer volume of institutional hedging creates a more stable, albeit thinner, funding environment. Traders must account for the fact that large market makers now dominate the order book, often narrowing the spread between exchanges faster than before. This requires tighter execution and lower fee structures to remain profitable.

The strategy is no longer just about capturing high yields; it is about managing the cost of carry against institutional liquidity. As ETFs absorb spot demand, the premium on perpetual futures can compress, forcing arbitrageurs to look for cross-exchange discrepancies or alternative assets where institutional penetration remains lower. The game has moved from picking low-hanging fruit to navigating a more efficient, competitive market.

Common questions about funding arb

How to execute a delta-neutral funding trade?

The core mechanic involves opening offsetting positions to eliminate directional risk. You buy spot assets while simultaneously shorting the equivalent amount in perpetual futures. This creates a delta-neutral portfolio where price movements don't affect your equity, isolating the funding rate payment as your sole variable for profit or loss.

Is funding rate arbitrage profitable?

Profitability depends entirely on the basis spread relative to your costs. You earn the funding rate if the market is in contango, but you must subtract trading fees, slippage, and capital costs from that yield. In bear markets, negative funding rates can turn a seemingly safe trade into a liability, making timing critical.

What is the primary risk in this strategy?

Exchange insolvency and withdrawal halts are the most severe risks. Since you hold assets across two platforms, if one exchange fails or freezes withdrawals, you cannot rebalance or close your hedge. Additionally, extreme volatility can trigger liquidations on your futures leg if margin is insufficient, even if your overall position remains profitable.

No comments yet. Be the first to share your thoughts!