Understanding funding rate mechanics

Funding rates are the mechanism exchanges use to tether perpetual futures prices to the underlying spot market. Without this system, perpetual contracts would drift away from the actual asset price, creating chaotic arbitrage opportunities that benefit no one but market makers. The funding rate acts as a periodic payment between traders, designed to keep the futures price in line with the spot price.

When the futures price trades above the spot price, the market is in contango. This signals that traders are aggressively buying leverage, pushing the price up. To correct this, the funding rate becomes positive. Long position holders must pay short position holders. This payment structure incentivizes traders to sell the futures contract (or buy the spot asset), which naturally brings the futures price back down toward the spot price.

Conversely, when the futures price falls below the spot price, the market is in backwardation. Here, the funding rate turns negative. Short position holders pay long position holders. This encourages traders to buy the futures contract, pushing the price back up. For arbitrageurs, this dynamic creates a predictable income stream. By holding a spot position and an opposite perpetual futures position, you can collect these payments regardless of where the asset price moves, provided the funding rate remains favorable.

This mechanism is not just theoretical; it is the backbone of crypto derivatives infrastructure. Exchanges like Binance and Bybit calculate these rates every eight hours, ensuring that the perpetual contract never deviates significantly from the spot market for long. Understanding this push-and-pull dynamic is essential for anyone looking to implement funding rate arbitrage strategies.

Key funding arb tools and platforms

You can’t run a funding arbitrage strategy blind. The spread between spot and perpetual futures is often razor-thin, and it changes with every funding interval. To catch these moves, you need reliable data aggregators for spotting the rates and execution engines for managing the positions.

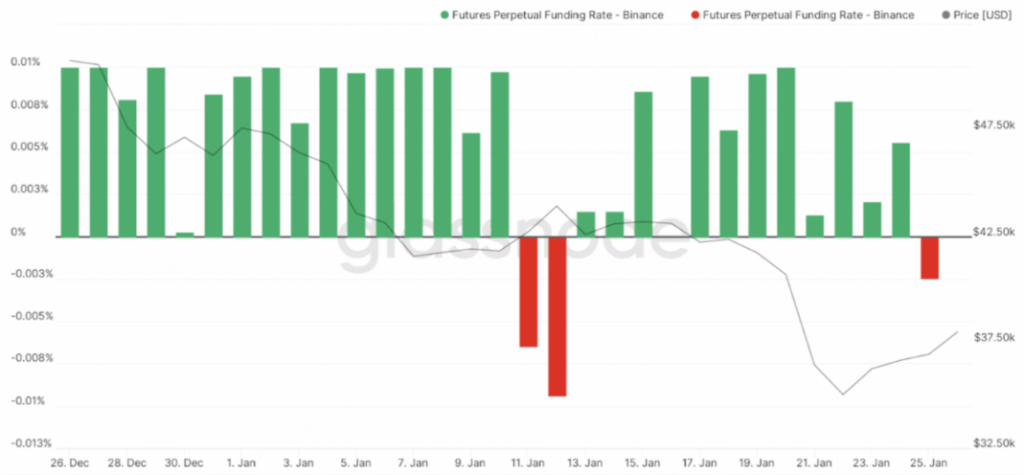

Data Aggregators: CoinGlass

Before you place a trade, you need to know where the yield is. CoinGlass provides a central dashboard for real-time funding rates across major exchanges. Their interface tracks the balance between long and short positions, giving you a clear view of which assets are trading at a premium or discount. You can filter by token or exchange to find the highest yields, but remember that high rates often signal high risk or low liquidity.

Execution Engines: Hummingbot

Once you’ve identified the opportunity, you need software to execute it. Hummingbot is an open-source framework that automates market-making and arbitrage strategies. Their community has developed specific strategies for funding rate arbitrage, allowing you to manage both the spot and futures legs of the trade simultaneously. This automation is critical because manual execution is too slow to capture the full spread before it narrows.

Custom Analysis: GitHub Repositories

For traders who need granular control, many rely on custom scripts hosted on GitHub. Repositories like SainyTK/funding-arb-analysis provide the raw tools to download historical funding data and price action from multiple exchanges. This approach lets you backtest strategies against your own risk parameters rather than relying on pre-packaged solutions. It requires more technical effort but offers the deepest insight into historical funding behavior.

| Tool | Type | Best For |

|---|---|---|

| CoinGlass | Data Aggregator | Real-time rate monitoring |

| Hummingbot | Execution Engine | Automated strategy deployment |

| GitHub Scripts | Custom Analysis | Backtesting and granular control |

Analyzing risk and return profiles

Funding rate arbitrage is often marketed as a risk-free yield strategy, but that label ignores the structural realities of the market. While the spread between spot and futures prices can generate steady income, the strategy exposes traders to three distinct categories of risk: liquidation, counterparty, and basis risk. Understanding these vulnerabilities is essential for capital preservation.

Liquidation risk

Even with a delta-neutral setup, liquidation remains the most immediate threat. If the underlying asset price moves sharply against your position, the margin in your account can be depleted before the hedge fully offsets the loss. This is particularly dangerous during periods of high volatility, where price gaps can occur faster than you can adjust your position. Monitoring your liquidation price and maintaining a healthy margin ratio is non-negotiable.

Exchange counterparty risk

Your capital is split across two exchanges: one for spot and one for futures. This creates a dual exposure to exchange solvency and operational integrity. If one exchange experiences a withdrawal halt, a hack, or a bankruptcy, your arbitrage loop is broken, and your funds may be inaccessible. Diversifying across reputable, regulated platforms and avoiding single-point failures can mitigate this, but it never eliminates it entirely. Always check the exchange’s proof of reserves and historical stability before deploying significant capital.

Basis risk

The funding rate is not static; it fluctuates based on market sentiment and liquidity. If the basis widens against you or collapses to zero, your expected return vanishes. In extreme cases, the funding rate can turn negative, forcing you to pay rather than receive fees. This risk is inherent in the strategy and requires active monitoring of market conditions. Tools like Coinglass or Presto Labs can help track these trends, but they cannot predict sudden market shifts.

Essential tools for risk management

To navigate these risks, you need robust infrastructure. Real-time data feeds, automated margin management, and cross-exchange monitoring tools are critical. Without them, you are trading blind. The following products represent essential hardware and software tools for serious arbitrageurs who need reliable, low-latency execution and secure storage solutions.

As an Amazon Associate, we may earn from qualifying purchases.

By acknowledging these risks and implementing proper safeguards, you can better position your funding arb strategy for long-term sustainability. The goal is not to eliminate risk, but to manage it with precision and discipline.

Infrastructure for capital efficiency

Funding rate arbitrage is a capital-intensive game. Your returns are determined by the spread between spot and futures, but your actual profitability is dictated by how efficiently you deploy that capital. If your funds are stuck in transit or sitting idle in margin accounts, the opportunity cost eats into your edge.

Modern infrastructure tools solve this by automating the movement and allocation of assets across exchanges. Instead of manually bridging funds or rehypothecating collateral, traders use integrated platforms to keep capital fluid. This reduces the friction that often turns a theoretically profitable spread into a net loss after fees and slippage.

Cross-exchange transfers

Speed matters. When a funding rate spikes, the window to enter the trade is narrow. Tools that offer instant cross-exchange transfers allow you to move capital between spot and derivatives accounts without waiting for blockchain confirmations on slow networks. This immediacy ensures you capture the rate before it normalizes.

Margin efficiency

Not all margin is created equal. Efficient infrastructure allows for cross-margin models where collateral from one position can support another, reducing the total amount of capital required to maintain open positions. By maximizing the utility of every dollar, you can scale your arbitrage strategies without proportionally increasing your exposure to market volatility.

How to execute a funding arb trade

Funding rate arbitrage relies on the spread between spot and perpetual futures prices. The core mechanic is simple: you buy the asset on the spot market while simultaneously shorting the same asset on the perpetual futures market. This delta-neutral structure isolates the funding rate payments as your primary source of return.

To structure this trade, you need a platform that supports both markets with low latency. Hummingbot, an open-source framework, is a common choice for automating this flow. Its Funding Rate Arbitrage strategy handles the synchronization of orders, ensuring your hedge remains tight even as prices fluctuate. You can watch a technical walkthrough of this setup in the Hummingbot CTO's deep dive.

Execution requires monitoring the funding interval. Rates typically pay out every eight hours. You must ensure your exchange accounts have sufficient margin on the futures side to avoid liquidation, even in a delta-neutral setup. A sudden spike in volatility can widen the spread, temporarily marking your futures position at a loss until the next funding payment offsets it.

Research assets with consistently positive funding rates. Use tools like Coinglass to verify that the rate is sustainable and not an anomaly driven by a short squeeze. Target tokens with high volume to ensure you can enter and exit the spot leg without slippage.

Purchase the underlying asset on your chosen spot exchange. Ensure you have enough capital to cover trading fees on both the buy and sell sides. Some traders use stablecoin pairs to avoid volatility risk on the base asset, while others prefer BTC or ETH for liquidity.

Immediately open a short position on the perpetual futures market for the same amount. Use isolated margin to contain risk. The goal is to lock in the funding rate differential. If the rate is negative, the strategy flips: you short spot and go long futures.

Funding rates change every interval. Regularly check the spread to ensure it remains profitable after accounting for trading fees and potential funding rate reversals. Rebalance your positions if the price moves significantly to maintain your delta-neutral status.

Funding rate arbitrage: what to check next

Funding rate arbitrage is a straightforward concept: borrow capital at a low interest rate and invest that money where it generates higher returns [src-serp-4]. Exchanges use these rates to keep futures prices consistent with spot prices, acting as an incentive for traders to balance long and short positions [src-serp-6]. While the mechanics are simple, execution requires careful market research to identify tokens with sustained positive rates.

No comments yet. Be the first to share your thoughts!