How funding rates create arb opportunities

Funding arbitrage, often called the "cash and carry" trade, exploits the mechanical divergence between perpetual swap prices and the underlying spot market. In a standard market, the price of a perpetual contract should track the spot price of the asset. However, because perpetuals have no expiration date, exchanges introduced a funding rate mechanism to tether the two prices together.

The funding rate is a periodic payment exchanged between long and short traders. When demand for long positions is high, the perpetual price trades at a premium to spot. In this scenario, longs pay shorts. Conversely, when shorts dominate, the perpetual trades at a discount, and shorts pay longs. This payment structure is the engine of the arbitrage opportunity.

The strategy itself is straightforward: you buy the asset on the spot market while simultaneously opening an equivalent short position on the perpetual swap. By holding both positions, you hedge out the directional price risk of the underlying asset. If Bitcoin drops, your spot position loses value, but your short position gains the same amount. The profit comes entirely from the funding payments you collect as the short side of the trade.

This spread is not static. It fluctuates based on market sentiment, leverage levels, and liquidity. During bull markets, positive funding rates can be substantial, offering attractive yields. In bear markets, rates can turn negative, allowing traders to profit by reversing the positions—shorting spot and going long on perps. The key is identifying when the spread is wide enough to cover trading fees and still provide a net positive return.

To execute this trade effectively, you need to monitor the funding rate clock and exchange liquidity. Most exchanges settle funding every eight hours. Missing a settlement window or facing insufficient liquidity on one side of the trade can erode profits or introduce slippage risk. Always verify the current rate across multiple venues before entering the position.

- Hedge Direction: Buy spot, short perpetual for positive funding; short spot, long perpetual for negative funding.

- Monitor Clock: Track settlement times to ensure you are positioned for the next payment cycle.

- Calculate Costs: Include trading fees, withdrawal fees, and funding payments in your yield calculation.

- Check Liquidity: Ensure sufficient depth on both spot and perpetual sides to enter and exit cleanly.

Execution models for 2026

Funding arbitrage in 2026 relies on two primary execution models: cross-exchange delta-neutral positioning and single-exchange basis trading. The choice between them depends on your infrastructure capabilities and the current rate models. Cross-exchange strategies offer higher potential yields but require managing custody and withdrawal risks across multiple platforms. Single-exchange strategies are simpler to execute but often face tighter margins due to internal competition.

Cross-exchange delta-neutral positioning involves buying spot on one exchange and selling perpetual futures on another. This isolates the funding rate differential as the sole source of profit. In 2026, this model is increasingly dominated by institutional players with direct API access and low-latency infrastructure. Retail traders often find it difficult to compete on speed and fee structures. The strategy requires careful monitoring of withdrawal limits and network congestion, which can disrupt the hedge if not managed precisely.

Single-exchange basis trading focuses on the spread between spot and perpetual prices on a single platform. This approach eliminates counterparty risk related to cross-exchange transfers but exposes traders to platform-specific risks. As rate models evolve, exchanges may adjust funding rate caps or calculation frequencies, directly impacting profitability. Traders must stay informed about these changes to adjust their positions accordingly. The simplicity of this model makes it accessible, but the margins are often thinner compared to cross-exchange opportunities.

Cross-Exchange vs. Single-Exchange Strategies

The table below compares the key characteristics of these two execution models.

| Feature | Cross-Exchange | Single-Exchange |

|---|---|---|

| Risk Profile | Higher (counterparty, transfer) | |

| Risk Profile | Lower (platform-specific only) | |

| Complexity | High (multi-platform management) | |

| Complexity | Low (single platform) | |

| Yield Potential | Generally higher | Generally lower |

| Infrastructure Needs | Advanced (APIs, monitoring) | Standard |

Infrastructure Requirements

Successful execution in 2026 demands robust infrastructure. This includes reliable API connections, real-time data feeds, and automated monitoring tools. Manual trading is rarely viable due to the speed at which opportunities arise and disappear. Traders must also consider the cost of capital and the efficiency of their funding rate collection mechanisms. As the market matures, the gap between professional and amateur execution widens, making infrastructure a critical differentiator.

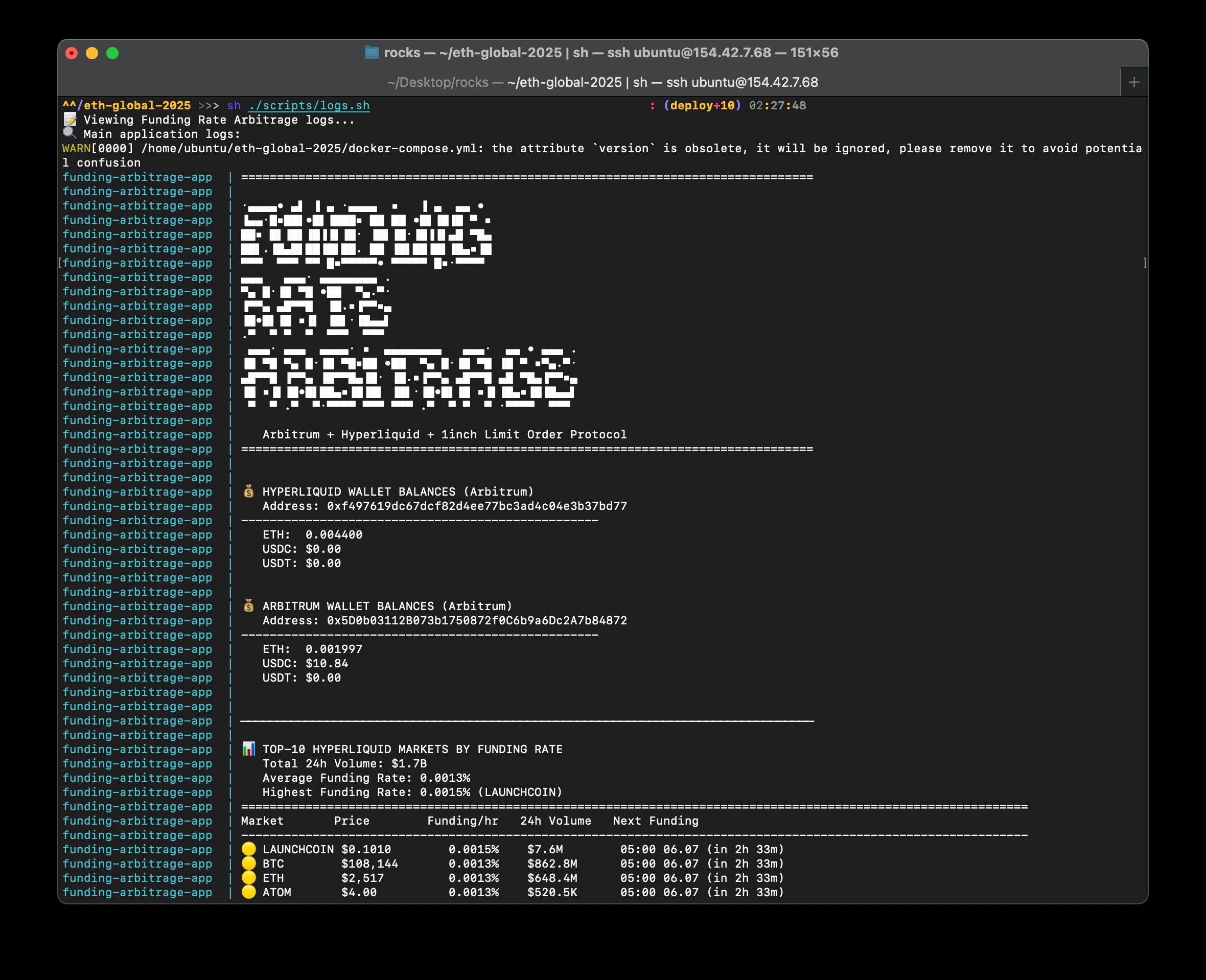

Essential tools for funding arb analysis

You cannot run a funding arbitrage strategy on gut feeling or delayed screenshots. In 2026, the spread between perpetual swaps and spot markets moves too fast for manual tracking. You need a stack that monitors real-time funding rates, tracks liquidity depth, and calculates execution costs before the opportunity disappears.

The foundation of this stack is a reliable data provider. Amberdata and similar infrastructure layers offer the API-level visibility needed to spot divergences across exchanges. Without this, you are trading blind. You need to see the funding rate not just as a number, but as a trend line against the asset's price action.

Execution requires more than just data; it requires speed. You need software that can calculate the net annualized percentage (APY) after accounting for trading fees and slippage. A rate that looks profitable on paper often turns negative once you factor in the cost to open and close the hedge. Look for tools that integrate directly with your exchange accounts to automate this calculation.

Liquidity is the silent killer of funding arb. Even if the rates are favorable, you need enough depth to enter and exit your position without moving the market. Tools that visualize order book depth and recent trade volume are essential. If the order book is thin, your entry and exit costs will eat your entire margin.

Building robust arb infrastructure

Capturing fleeting funding rate spreads requires more than just identifying the right tokens; it demands a technical stack built for speed and stability. In 2026, the latency gaps between major venues are shrinking, meaning manual execution is no longer viable. You need infrastructure that can monitor multiple order books simultaneously and execute trades with minimal slippage.

API Management and Connection Stability

Your API connections are the lifeline of your strategy. Exchange rate limits are strict, and a dropped connection can mean missing a funding payment window or being unable to close a hedge during volatility. Implement robust retry logic and monitor your API health in real-time. A single timeout during a market swing can turn a risk-free arb into a directional exposure.

Low-Latency Execution

Speed is the primary edge in funding arbitrage. You need to execute the long and short legs of your trade nearly simultaneously to avoid basis risk. This often requires co-located servers or direct market access (DMA) where available. Even milliseconds matter when the spread narrows quickly.

Capital Allocation Across Venues

Efficient capital deployment is critical. You must allocate liquidity across exchanges to maximize yield while minimizing idle cash. Use a centralized ledger to track margin requirements and available balances across all venues. This ensures you can rebalance positions instantly without waiting for internal transfers between exchanges.

Navigating new exchange rate models

The 2026 landscape for funding rate arbitrage is defined by structural shifts. Major exchanges have moved away from simple time-weighted averages toward dynamic, volatility-adjusted models. These changes were designed to prevent rate manipulation during extreme market swings, but they fundamentally alter the predictability of funding streams.

Traders can no longer rely on static historical averages to project future cash flows. A high funding rate today may decay faster than expected if the new model detects excessive leverage buildup. Your risk models must now incorporate real-time order book depth and volatility metrics to accurately price the duration of a funding position.

Adapting your infrastructure means prioritizing low-latency data feeds that capture these model updates instantly. If your execution layer cannot react to sudden rate recalibrations, the spread between spot and perpetual markets may vanish before you can hedge. Success now depends on agility, not just capital allocation.

Frequently asked questions about funding arb

How to do funding rate arbitrage?

To execute funding rate arbitrage, you need to identify assets with persistently high positive funding rates and short them on the perpetual futures market while holding the underlying spot asset. This requires rigorous market research to ensure the rate remains positive long enough to cover borrowing costs and capture the spread.

What are the main risks in 2026?

Infrastructure changes in 2026 have increased the complexity of liquidation risks. Smart contract vulnerabilities and exchange solvency issues remain primary concerns. Additionally, rapid funding rate shifts can erode margins if your hedge position moves against you before the next settlement.

Is funding arbitrage profitable?

Profitability depends on the net funding rate minus trading fees and slippage. While the strategy is theoretically risk-free, execution costs often eat into returns. Successful traders focus on high-volume pairs with consistent premium structures to maintain positive carry.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!