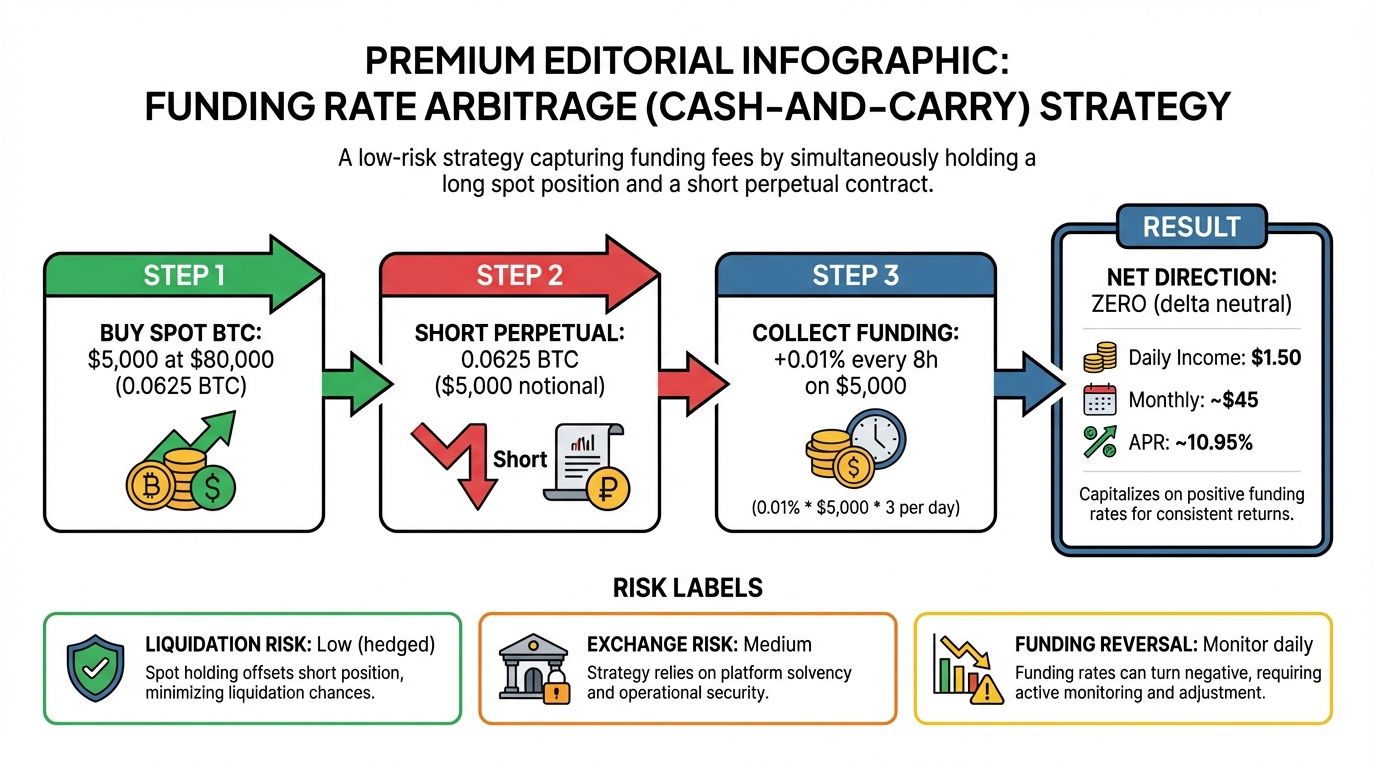

How funding rate arbitrage works

Funding rate arbitrage is a market-neutral strategy designed to capture the spread between two exchanges without betting on price direction. The core mechanic is simple: you go long on the exchange with negative funding rates and short on the exchange with positive funding rates. This setup allows you to collect periodic payments while hedging your exposure to the underlying asset.

Think of it like a bond yield spread. You borrow at a low rate and lend at a higher rate. In crypto perpetual futures, the "interest" is the funding rate. When you hold a long position on an exchange where funding is negative, you actually receive payments from short sellers. Conversely, if you hold a short position where funding is positive, you pay those same fees. By balancing these positions across two venues, the price movements cancel each other out, leaving only the funding differential as your profit or loss.

This approach is often called a "cash-and-carry" trade in traditional finance, but in crypto, it happens entirely on derivatives markets. The goal is to exploit inefficiencies where one exchange is more bullish than another. As Amberdata notes, the strategy relies on capturing these rate differentials while maintaining a hedged book. The risk isn't that Bitcoin moves up or down; it's that the spread between the two exchanges narrows or reverses unexpectedly.

To execute this safely, you need to monitor the funding intervals carefully. Most exchanges settle every eight hours, but some, like Hyperliquid, settle every hour. A mismatch in settlement timing can introduce basis risk, where the price divergence between exchanges widens faster than the funding payments can compensate. Always verify the current rates on both platforms before entering the trade.

Step 1: Find profitable rate differentials

You cannot execute a funding arb if the spread doesn't cover your costs. The first step is scanning for positive funding spreads between exchanges. You are looking for a situation where the difference between the high-paying exchange and the low-paying exchange is large enough to absorb trading fees, withdrawal costs, and the risk of price movement.

Start by using a dedicated scanner like Arbitrage Scanner or CoinGlass to compare real-time rates. These tools aggregate data from major platforms, allowing you to spot discrepancies quickly. Look for pairs where one exchange offers a significantly higher funding rate than another for the same asset.

A positive spread means you can go long on the exchange with the lower rate and short on the one with the higher rate. However, the spread must exceed your fees. If the difference is only 0.01% but your trading fees total 0.02%, you are losing money on every cycle. Always calculate the net profit after all costs before placing any orders.

High-stakes risk: Margin trading introduces liquidation risk. If the market moves sharply against your short or long position, you could lose more than your initial capital. Ensure your leverage is managed carefully.

Once you identify a viable spread, verify the data across multiple sources. Funding rates can change rapidly, often every 8 hours. What looks profitable now might disappear in minutes. Use official exchange APIs or reputable aggregators to confirm the current rate before committing funds.

Step 2: Set up hedged positions

Now that you have identified a viable spread, the next phase is execution. The goal here is to lock in the funding rate differential while neutralizing the risk of the underlying asset's price moving against you. This requires opening two positions simultaneously: a long position on the exchange with the positive funding rate, and a short position on the exchange with the negative (or lower positive) funding rate.

Think of this like holding a balance scale. If you only hold one side, the weight of the market price movement can tip the scale and wipe out your profits. By holding both sides in equal measure, you create a delta-neutral portfolio. The gains or losses from the price movement on one exchange are offset by the opposite movement on the other. Your profit comes almost entirely from the funding payments exchanged between the two venues, not from the asset's price direction.

To execute this safely, you must manage your margin correctly on both sides. Margin trading introduces leverage, which amplifies both potential returns and the risk of liquidation. If one exchange experiences a sudden price spike while the other remains static, your margin requirements may shift. You must ensure that both positions have sufficient isolated or cross-margin to withstand volatility. A common mistake is under-collateralizing one leg, leading to a forced liquidation that breaks the hedge and leaves you exposed to market risk.

Select the exchange where the funding rate is positive. Open a long perpetual futures position for the target asset. Ensure the position size matches your intended capital allocation. This leg will receive the funding payments every 8 hours (or whatever the interval is for that exchange).

Immediately open a short perpetual futures position on the second exchange. The size must be identical to the long position to maintain neutrality. This leg will pay the funding rate. The difference between what you receive and what you pay is your gross arbitrage profit.

Check the maintenance margin requirements on both exchanges. High leverage reduces the capital needed but increases liquidation risk. For funding arbitrage, lower leverage (e.g., 2x-5x) is generally safer to absorb price swings. Ensure you have enough free margin to cover potential mark-price fluctuations.

Set up alerts for funding rate changes and price divergence. While the hedge protects against directional risk, the spread between exchanges can widen or narrow. If the spread moves against you significantly, you may need to adjust positions or exit early to preserve capital.

As an Amazon Associate, we may earn from qualifying purchases.

This simultaneous execution is critical. If you open one leg and wait before opening the other, you are exposed to market risk during that window. Use limit orders or pre-configured bots if available to minimize the time between legs. The tighter the execution, the more predictable your arbitrage profit will be.

Manage margin and liquidation risk

Even when you are hedged, funding arbitrage is not immune to liquidation. The danger does not come from the asset price moving against you—it comes from the exchange’s maintenance margin requirements and the timing of your cash flows. If your collateral balance dips below the required threshold on either leg of the trade, the exchange will liquidate your position, turning a theoretically risk-free trade into a realized loss.

Monitor maintenance margin closely

Every exchange sets a maintenance margin level, which is the minimum equity you must hold to keep a position open. This is not a static number; it often scales with your position size and market volatility. During high volatility, exchanges may raise these requirements abruptly. If your collateral is tied up in the long leg but the short leg requires more margin due to a spike in volatility, you could face a margin call on the short side even if your net exposure is neutral.

You must track the maintenance margin on both exchanges simultaneously. Do not assume that because you are hedged, you are safe. The hedge protects against price direction, but it does not protect against exchange-specific margin hikes. Keep a buffer of free collateral that exceeds the maintenance requirement by a comfortable margin—aim for at least 20-30% headroom to absorb sudden spikes.

Handle basis risk and timing

The basis—the difference between the spot and futures price—can widen or narrow unpredictably. While this is the source of your profit, it also introduces risk if you need to close positions early. If you are forced to exit due to a margin call, you might have to close at an unfavorable basis, eroding your profit or causing a loss.

Additionally, be aware of withdrawal halts or exchange insolvency risks. A hedged position is only as safe as the platforms holding your assets. If one exchange freezes withdrawals during a crisis, you cannot move collateral to cover the other leg.

Use a margin calculator

Before entering the trade, use a margin calculator to determine the exact collateral needed on both sides. Factor in the worst-case scenario for maintenance margin increases. This ensures you have enough free cash to survive volatility without triggering a liquidation.

Common mistakes that kill funding arb profits

Cross-exchange funding rate arbitrage looks like free money on paper, but the execution is where most traders bleed capital. Even with a positive spread, a single overlooked variable can turn a theoretical gain into a net loss. The strategy relies on precision, not just timing.

Ignoring the fee drag

Funding payments are recurring, but trading fees are immediate. If you forget to factor in maker/taker fees, deposit charges, or withdrawal costs, your net profit vanishes. A 0.01% funding rate sounds attractive until you realize the spread is eaten by the 0.02% round-trip trading cost. Always calculate the breakeven spread before entering the position.

Mismatched contract sizes and leverage

You cannot hedge perfectly if your positions are not equal in dollar value. If you are long $10,000 of BTC on Exchange A but only short $9,000 on Exchange B, you are exposed to directional risk. If the price moves against your larger position, the funding income will not cover the liquidation risk. Ensure your notional values match precisely, accounting for leverage differences.

Withdrawal and transfer risks

The biggest silent killer is liquidity delay. If you need to move collateral between exchanges to cover a margin call or rebalance, network congestion or exchange maintenance can freeze your funds. During a volatile market move, being unable to transfer assets in time can lead to liquidation on one side of the trade. Always keep sufficient buffer capital on both sides to avoid forced closures.

-

Verify total fees (trading + withdrawal) are less than expected funding spread

-

Confirm notional values of long and short positions are equal

-

Ensure sufficient buffer capital exists on both exchanges to cover margin calls

Frequently asked questions about funding arb

Funding arbitrage sounds simple in theory, but the execution requires precision. Here are the most common questions traders ask when trying to execute a funding arb guide strategy.

No comments yet. Be the first to share your thoughts!