Set up your delta-neutral positions

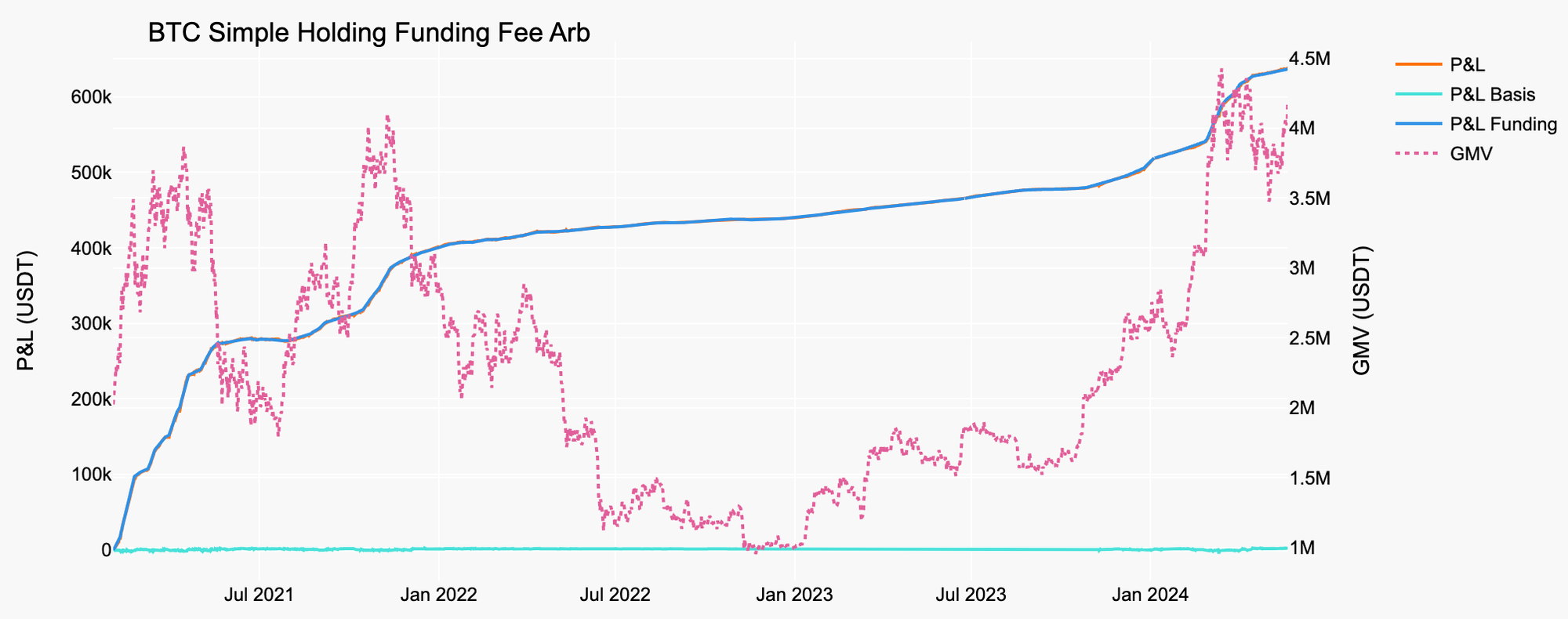

To execute funding rate arbitrage, you need to lock in the premium paid by leveraged traders. The core mechanic is simple: you hold a long position in spot crypto and a short position in futures of equal value. This creates a delta-neutral portfolio, meaning your net exposure to price direction is zero. You are not betting on Bitcoin going up or down; you are collecting the funding fees paid by the short side of the market.

Think of this like running a bond fund. You aren't trying to guess the market's next move. You are providing liquidity to traders who want leverage, and the funding rate is your interest payment. However, unlike a savings account, crypto futures are perpetual. If the market moves violently against your short hedge, you face liquidation risk, even if your spot holdings are safe. Precision in sizing and execution is non-negotiable.

Buy the underlying asset (e.g., BTC or ETH) on your spot exchange. This is your collateral base. Ensure you have enough balance to cover both the spot purchase and the margin required for the futures short. Use a major exchange with deep liquidity to minimize slippage on entry.

Open a short position on the futures market for the same amount of crypto. For example, if you bought $10,000 worth of BTC spot, open a $10,000 notional short on BTC perpetual swaps. Match the contract type (e.g., USDT-Margined) to your spot holdings. This short position will profit if the price drops, offsetting the loss in your spot holdings.

Check your net exposure. Your spot delta should be +1 (or +100%) and your futures delta should be -1 (or -100%). The sum should be zero. If you are using leverage, ensure your margin ratio is healthy. A common mistake is under-collateralizing the short, which leaves you exposed to liquidation if the price spikes up.

Once your positions are live, the funding rate clock starts. Funding payments typically occur every 8 hours. If the funding rate is positive, long traders pay short traders. Since you are short, you receive these payments. This is your yield. However, this yield is not risk-free. As noted by industry analysts, extreme price movements can trigger liquidation on the futures leg if your margin is insufficient, wiping out your spot gains. Always monitor your margin ratio closely.

Calculate expected annualized yield

Turning a raw funding rate into a realistic APY requires two steps: annualizing the periodic payment and subtracting the friction costs. Ignoring either part turns a theoretical profit into a real loss.

1. Annualize the rate

Funding payments occur every eight hours on most major exchanges, meaning you receive (or pay) a rate three times daily. To project this over a year, multiply the periodic rate by 3, then by 365.

For example, a 0.01% funding rate paid every eight hours results in an annualized figure of 10.95% (0.0001 × 3 × 365). This number represents the gross yield before any costs are deducted.

2. Subtract trading fees

Trading fees destroy high-frequency strategies. You must account for the maker and taker fees on both the long and short legs of your position. A typical round trip—opening and closing both positions—can cost 0.02% to 0.08% depending on your exchange tier and volume.

Subtract the total round-trip fee percentage from the annualized rate. If your fees are charged per transaction, multiply by the number of rebalancing cycles you expect to execute in a year.

3. Account for funding drift

The rate you see today is not the rate you will receive tomorrow. Funding rates fluctuate based on market sentiment and liquidity. A strategy that looks profitable at 10% APY today might drop to 4% APY next week if the market cools off.

Always stress-test your calculations using historical lows rather than current highs. If the strategy becomes unprofitable at a 50% historical average, it carries significant downside risk. Only proceed if the net yield remains positive under conservative estimates.

Manage liquidation risk on the short leg

In funding arbitrage, your short position is the weak link. While the long leg earns yield, the short leg is exposed to the market. If prices spike during a bull run, your short position loses value rapidly. This is not just a paper loss; it is a margin call waiting to happen. Unlike a long position that can wait for a recovery, a short position can be liquidated before the market turns back down.

Think of your margin like a safety net. If the net is too tight, any sudden jump in price snaps the ropes. The risk is highest when volatility spikes, as funding rates often rise alongside price, squeezing your margin from both sides. You need enough buffer to survive the worst-case scenarios without getting wiped out.

To protect your capital, you must manage your margin ratio carefully. Here is how to structure your positions to survive the squeeze.

The goal is to survive the volatility, not to predict it. By keeping your margin ratio healthy and using isolated margin, you protect your long leg from the short leg's risks. This is the only way to ensure your funding arbitrage strategy remains profitable over the long term.

Track funding rates across exchanges

To find genuine arbitrage opportunities, you need real-time data from multiple sources. Funding rates shift constantly as market sentiment changes. Relying on a single exchange’s dashboard is like trying to navigate a storm with one eye closed. You must compare rates across at least three major platforms to spot the widest spreads.

We recommend using dedicated scanners that aggregate this data. These tools save you from manually refreshing five different tabs. They highlight where the premium is highest, allowing you to act before the spread narrows. Accuracy is non-negotiable here; a lagging data feed can turn a profitable trade into a liquidation event.

The table below compares the most reliable tracking tools. Each offers different strengths, from speed to historical depth. Choose the one that fits your workflow, but never rely on just one.

| Tool | Update Speed | Exchange Coverage | Cost |

|---|---|---|---|

| Coinglass | Real-time | 50+ Exchanges | Free/Premium |

| Amberdata | Near real-time | Major Tier-1 | API Subscription |

| ArbitrageScanner | Live | Top 10 Pairs | Free Tier |

| Binance Data | Instant | Binance Only | Free |

If you prefer a more hands-on approach, you can also monitor official exchange APIs. This method requires more technical setup but provides the most raw, unfiltered data. For those who want a curated list of hardware to help manage multiple monitors and data feeds while tracking these rates, consider checking out these essential setup items.

As an Amazon Associate, we may earn from qualifying purchases.

Common mistakes in funding arb

Even with a perfectly delta-neutral setup, funding rate arbitrage can bleed capital if you treat it as passive income. The strategy looks safe on paper because your directional exposure is hedged, but the ledger tells a different story. You are trading a spread, and spreads can turn negative faster than you can react.

Ignoring fees and slippage

Many traders calculate the net yield by subtracting the funding payment from the funding receipt, but they forget the friction costs. Trading fees, withdrawal fees, and the bid-ask spread (slippage) eat into that margin. If the spread is thin, a single trade might cost more in fees than the funding payment earns. Always run a full cost simulation before entering.

Miscalculating leverage

Leverage amplifies both gains and liquidation risks. In funding arb, you are often using leverage to boost yields on small spreads. If one side of your hedge moves sharply against you, the unhedged portion (caused by imperfect correlation or fee mismatches) can trigger a liquidation cascade. Keep leverage conservative and monitor your margin ratio closely.

Failing to monitor position size

Market conditions change. A high funding rate today might drop to near zero tomorrow, or worse, flip negative. If you have allocated too much capital to a single pair, you might find yourself stuck in a losing position with no easy exit. Diversify across multiple pairs and keep position sizes small enough to adjust quickly.

Pre-trade checklist

Before you execute, run through this list to avoid common pitfalls:

-

Calculate total fees (trading, withdrawal, network) against expected yield

-

Verify leverage ratio and margin requirements for both legs

-

Check the funding rate trend and historical volatility

-

Ensure you can exit both positions simultaneously if needed

-

Confirm the spread is positive after all costs are deducted

Funding arbitrage: what to check next

Funding arbitrage is a mechanical process, not a magic money printer. It relies on borrowing capital at a low interest rate to invest where it generates higher returns through funding fees (WunderTrading). While the math can look simple, the execution carries real risks that can wipe out your account if you aren't careful.

Is funding rate arbitrage profitable?

Yes, but it is not risk-free. Funding arbitrage can provide stable income, but it carries risks (CoinGlass). In extreme situations, when prices spike in either direction, there is a risk of liquidation for the other side of the position. You must monitor your margin closely, as a sudden market move can trigger a cascade even if your funding rate exposure is neutral.

How to do funding rate arbitrage?

The classic cross-exchange method involves opening opposing positions on two different platforms. For example, you might go long on Binance and short on Hyperliquid to capture the spread between their funding rates. However, not all spreads are profitable. If you pay more in funding fees than you receive, the trade is unprofitable as structured. You must calculate the net spread after fees before entering.

Is arbitrage possible for beginners?

For beginners, hunting for pure arbitrage in major markets is nearly impossible (VT Markets). Highly efficient markets like the New York Stock Exchange are dominated by algorithms. However, less efficient markets, like certain cryptocurrency exchanges or smaller international stock exchange platforms, still offer occasional opportunities. The crypto space is fragmented enough that a disciplined beginner can find edges, but it requires more effort than in traditional finance.

No comments yet. Be the first to share your thoughts!