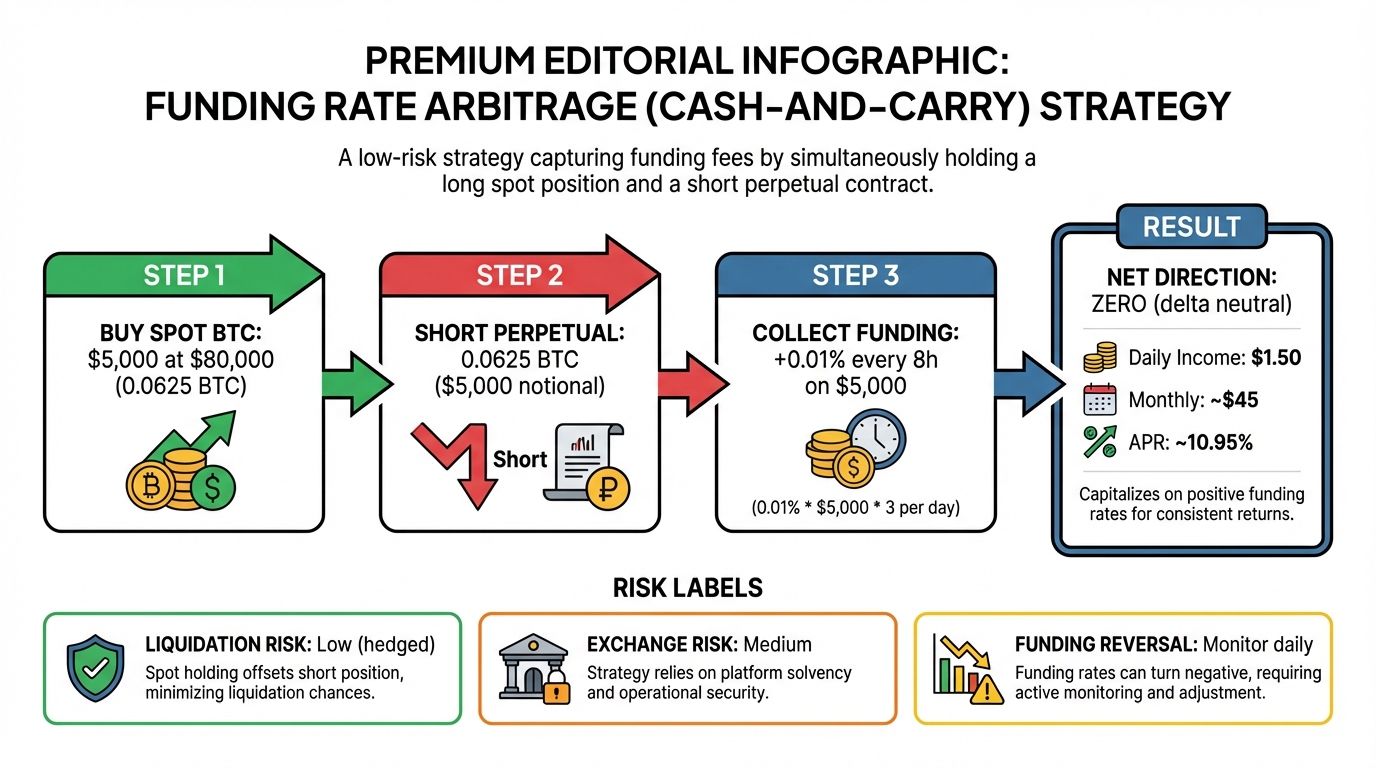

How funding rate arbitrage works

Funding rate arbitrage is a market-neutral strategy designed to profit from the premium paid by leveraged traders, rather than from the underlying asset's price direction. The core mechanism is simple: you simultaneously buy the asset on the spot market and open an equivalent short position on the perpetual futures market. This creates a "hedged" portfolio where your exposure to price movements cancels out.

The profit comes from the funding rate itself. In crypto perpetual contracts, funding rates are periodic payments exchanged between long and short traders to keep the futures price tethered to the spot price. When the market is bullish and longs are paying shorts, your short position receives these payments. By holding the spot asset (which appreciates with the market) and the short position (which collects funding), you isolate the funding yield as your primary return.

This structure is often mistaken for "free money" because the directional risk is theoretically neutral. However, it is not risk-free. The strategy relies on the stability of the exchange mechanics and the consistency of the funding spread. If the funding rate turns negative—or if the spread between spot and perp widens unexpectedly—the cost of carrying the positions can erode profits. You are essentially selling insurance to leveraged traders, collecting premiums while managing the risk of exchange-specific failures or liquidation cascades.

Cross-exchange vs single-exchange execution

Funding arb strategy execution boils down to where you hold your positions. Traders generally choose between cross-exchange arbitrage and single-exchange execution. The choice dictates your yield potential, operational complexity, and exposure to counterparty risk.

Cross-exchange arbitrage remains the standard for serious capital deployment. By holding spot on one exchange and shorting perpetual futures on another, you capture the full funding spread without relying on internal exchange incentives. This model separates your trading venues, meaning a liquidity crunch or API failure on one platform does not immediately liquidate your entire portfolio. However, it requires managing two accounts, two sets of fees, and the logistical friction of moving assets between platforms.

Single-exchange execution, often called "internal funding," simplifies the workflow. You hold spot and short futures on the same platform. While this eliminates withdrawal fees and transfer delays, it concentrates risk. If the exchange halts withdrawals or faces insolvency, your entire position is trapped. Also, some exchanges artificially suppress or manipulate funding rates for internal hedging, which can compress spreads and reduce yield compared to the open market.

Execution Comparison

The table below compares the primary mechanics of each approach.

| Feature | Cross-Exchange | Single-Exchange |

|---|---|---|

| Yield Potential | Higher (full market spread) | Lower (internal/subsidized) |

| Counterparty Risk | Diversified across venues | Concentrated on one venue |

| Operational Cost | Higher (withdrawal fees, transfers) | Lower (no transfers needed) |

| Complexity | Higher (multi-platform management) | Lower (single dashboard) |

| Liquidity Risk | Lower (independent liquidity pools) | Higher (shared pool exposure) |

When to Use Which Model

Choose cross-exchange execution if your priority is maximizing risk-adjusted returns and you have the operational capacity to manage multiple platforms. This is the preferred method for institutional and serious retail traders seeking to isolate themselves from single-venue failure modes.

Opt for single-exchange execution only if you are testing a strategy with small capital or if you have high conviction in the exchange's solvency and operational stability. The convenience comes at the cost of yield and increased systemic risk.

Tools for Execution

Successful execution requires reliable infrastructure. You need robust API access, low-latency order routing, and real-time monitoring of funding rates across venues. While specific software recommendations vary by trader preference, having a reliable scanner to track inter-exchange spreads is essential for identifying profitable opportunities.

As an Amazon Associate, we may earn from qualifying purchases.

Market Context

Understanding the current funding rate environment is critical for timing your entries. Funding rates fluctuate based on market sentiment, leverage demand, and liquidity conditions.

Infrastructure and Tooling

Executing a funding arb strategy requires more than just capital; it demands a robust technical stack to manage risk across multiple venues. The spread between spot and futures prices can vanish in seconds, meaning manual execution is rarely viable for consistent returns. You need infrastructure that can monitor rates and execute trades with minimal latency.

API connectivity is the backbone of this operation. Most professional traders use direct API connections to major exchanges like Binance or Bybit to access real-time order book data and execute trades programmatically. This allows for the simultaneous opening of long spot and short futures positions, which is the core mechanic of the strategy. Without reliable API access, slippage and execution delays can erase potential profits.

Note: The technical barrier to entry for retail traders is significant. While institutions use collocated servers and custom algorithms, retail traders must rely on exchange APIs and third-party monitoring tools, which introduces latency risks.

Monitoring software is equally critical. You need a centralized dashboard that aggregates funding rates across different exchanges and timeframes. Tools like Arbitrage Scanner provide real-time data on rate differentials, helping you identify the most profitable opportunities. These platforms often include calculators to estimate net returns after fees, allowing you to filter out trades that don't meet your risk-adjusted return criteria.

Capital allocation across multiple venues is the final piece of the puzzle. Diversifying your capital across several exchanges reduces counterparty risk and ensures you can always access the necessary liquidity. However, this also means managing multiple accounts, balances, and withdrawal limits. Effective tooling helps streamline this process, allowing you to track your total exposure and margin utilization across all venues from a single interface.

Managing basis risk and liquidation

The core tension in funding rate arbitrage is that you are collecting income while holding a short position that bleeds value during a bull market. While positive funding rates provide a steady stream of yield, the short perpetual futures contract is exposed to direct price risk. If Bitcoin pumps, your short position loses money on the mark-to-market value, even as you continue to collect funding payments.

This dynamic creates a scenario where the "free money" narrative often collapses under market volatility. Research into the risk and return profiles of this strategy confirms that while it can generate consistent returns in sideways or bearish markets, the underlying capital is still subject to significant drawdowns during sharp upward moves [src-serp-2]. The funding income must be high enough to offset the price appreciation of the asset, or the strategy results in a net loss despite the positive carry.

Liquidation risk adds another layer of complexity. Perpetual futures are leveraged instruments, and if the market moves against your short position rapidly, you may face a margin call or liquidation before the funding payments can accumulate enough to cover the loss. This is particularly dangerous if you are over-leveraged to boost the yield on your spot holdings. The strategy requires careful monitoring of your margin ratio and the funding rate trend, rather than a set-and-forget approach.

The following chart illustrates how price action can diverge from funding rates, highlighting the periods where basis risk is most acute.

Execution Checklist

Before deploying capital, run through this mental model. Funding arb is not free money; it is a risk-adjusted return that requires strict discipline. Treat the checklist as your gatekeeper.

Calculate the net yield after fees. Subtract trading fees, withdrawal costs, and potential slippage from the expected funding rate. If the spread doesn't cover these costs comfortably, skip the trade.

Only use exchanges with a proven track record of solvency. A counterparty default wipes out years of funding income. Diversify across two reputable platforms rather than concentrating risk on one.

Understand the maintenance margin for your short position. If the market spikes against your hedge, you need enough collateral to avoid liquidation before the next funding payment.

Define your exit conditions upfront. If the spread narrows below your threshold or the market moves violently, have a plan to close both legs simultaneously to lock in or cut losses.

Funding rate arbitrage: what to check next

Cross-exchange funding rate arbitrage involves buying an asset on a spot market while simultaneously shorting the same asset on a futures exchange to collect periodic funding payments. This strategy isolates the funding fee differential from directional price risk, though it is not without operational friction.

Is funding rate arbitrage considered risk-free?

No. While the market risk is hedged, you face basis risk if the spread between spot and futures widens unexpectedly. There is also counterparty risk; if an exchange halts withdrawals or experiences a liquidity crisis, your capital may be locked. Additionally, funding rates can turn negative, requiring you to pay rather than receive fees during certain market conditions.

What are the main costs that eat into profits?

Profits are eroded by trading fees on both the spot purchase and the futures short. You must also account for withdrawal fees when rebalancing positions across exchanges. The most significant hidden cost is slippage; executing large orders simultaneously on two different venues can move the market against you, reducing the initial spread advantage.

How often are funding payments made?

Most major crypto exchanges distribute funding payments every eight hours. This frequency means you need to maintain your hedge continuously to capture these payments. If you miss a payment window due to maintenance or technical issues, you lose that segment of the expected yield without any offsetting gain.

No comments yet. Be the first to share your thoughts!