What funding rate arbitrage actually is

Funding rate arbitrage is a market-neutral strategy that profits from periodic payments exchanged between long and short traders on perpetual futures contracts. The core mechanic is simple: you buy the underlying asset on the spot market while simultaneously opening an equal-sized short position on the perpetual futures market.

Because your positions are offsetting, your exposure to the asset's price movement is effectively neutralized. Whether Bitcoin goes up or down, the gain on one side is canceled by the loss on the other. Instead of betting on direction, you are betting on the funding rate itself.

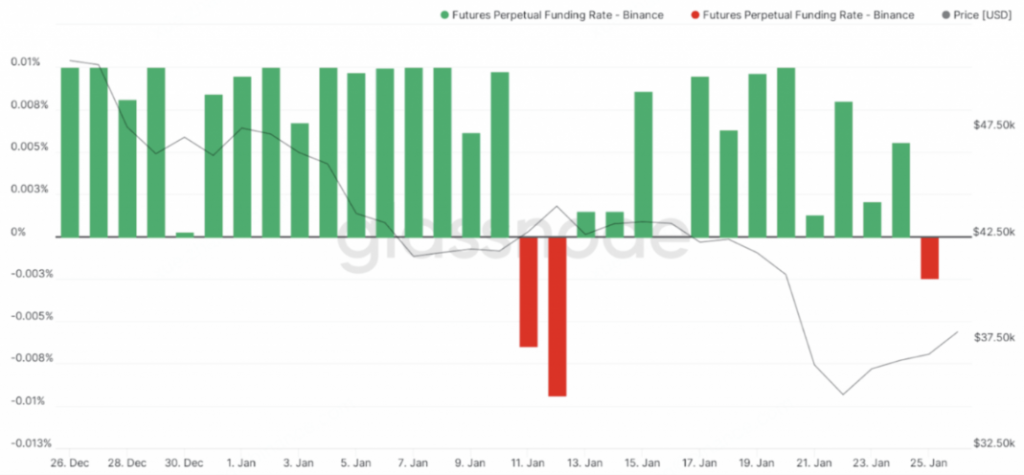

Perpetual futures contracts do not expire. To keep their price tethered to the spot price, exchanges use a mechanism called the funding rate. This is a periodic payment transferred between traders. When the market is bullish, longs pay shorts. When the market is bearish, shorts pay longs. In a funding arb setup, you hold the short position, meaning you collect these payments from the long traders.

Think of it like this: you are essentially renting out your crypto to the leveraged traders who are aggressively betting on the price going up. You provide the collateral (your spot holdings) and they pay you a fee to keep their leveraged positions open.

This structure makes funding arb attractive because it generates yield regardless of market direction. However, it is not risk-free. The strategy relies on the funding rate remaining positive and the price gap between spot and futures (the basis) staying stable. If the market flips bearish, the payment direction reverses, and you could end up paying the longs instead of receiving from them.

Why infrastructure matters for arb sustainability

Funding arb used to be a high-friction game of manual execution and constant vigilance. Traders had to manually roll positions, monitor margin ratios across different exchanges, and hope their funding rate predictions held up. The margin for error was slim, and the operational overhead was steep. Modern DeFi infrastructure has shifted that dynamic. It’s no longer just about picking the right token; it’s about leveraging the tools that make the strategy sustainable.

Cross-margin accounts and unified margin systems have been the biggest game-changers. In the past, maintaining a delta-neutral position required locking up significant capital in separate wallets or accounts to cover liquidation risks. Unified margin allows traders to use the same collateral across spot and derivatives markets. This efficiency reduces the capital required to enter a position, improving the effective yield of the arb. It also simplifies risk management, as a single margin pool absorbs the volatility of both legs of the trade.

Automated bots have further reduced the friction. Funding rates can change rapidly, and manual rebalancing often leads to missed opportunities or slippage. Bots can monitor rates, execute trades, and manage positions with a speed and precision that humans simply can’t match. This automation allows traders to scale their operations without a proportional increase in labor. It turns funding arb from a part-time job into a more passive, systematic process.

These infrastructure improvements don’t eliminate risk, but they make the strategy more accessible and robust. You’re no longer fighting the mechanics of the exchange; you’re leveraging them. For anyone serious about funding arb, understanding these tools is just as important as understanding the rates themselves.

Comparing exchange structures for funding arb

Your choice of exchange dictates the mechanics of your funding arb. It’s not just about which platform offers the highest rate; it’s about how that rate interacts with your capital and execution speed. Centralized exchanges (CEX) and decentralized exchanges (DEX) operate on fundamentally different models, impacting everything from fee structures to counterparty risk.

Centralized vs. Decentralized Execution

CEX platforms like Binance or Bybit offer high liquidity and fast settlement, making them ideal for capturing short-term rate spikes. However, they require trust in a centralized entity to hold your funds. DEXs like dYdX or GMX offer non-custodial trading, reducing counterparty risk, but often suffer from lower liquidity and higher slippage, which can erode your arb profits.

Unified vs. Segregated Margin

Inside CEXs, the margin model matters. Unified margin allows you to use assets across different products (spot, futures, options) as collateral, improving capital efficiency. Segregated margin isolates positions, reducing the risk of cross-product liquidations but tying up more capital. For funding arb, unified margin is often preferred to maximize leverage on your arbitrage positions without over-allocating funds.

Key Trade-offs at a Glance

The table below summarizes the core differences. Understanding these trade-offs helps you select the right structure for your specific funding arb strategy.

| Feature | CEX | DEX | Unified Margin |

|---|---|---|---|

| Execution Speed | High | Variable | N/A |

| Liquidity | High | Lower | N/A |

| Counterparty Risk | High (Centralized) | Low (Non-custodial) | N/A |

| Capital Efficiency | High (Cross-collateral) | N/A | High |

| Fee Structure | Maker/Taker fees | Gas + Protocol fees | N/A |

When building your funding arb guide, prioritize exchanges that align with your risk tolerance. If speed and liquidity are paramount, CEXs with unified margin offer the best infrastructure. If minimizing counterparty risk is your goal, DEXs provide a safer, albeit less efficient, alternative. Always verify current funding rates on platforms like Arbitrage Scanner before committing capital.

Key risks in funding rate arbitrage

It is easy to fall into the trap of thinking funding rate arbitrage is a guaranteed win. The strategy is often marketed as "market neutral," but that label is misleading. While you are hedging your directional exposure, you are still sitting in the middle of a volatile storm. Market neutral does not mean risk-free; it just means you aren't betting on the price going up or down. You are betting on the funding rate staying favorable, and that is a much riskier bet than it appears.

Liquidation risk

The biggest threat to your capital is liquidation. Even with a perfect hedge, a sudden, sharp move in the underlying asset can trigger a margin call on one side of your trade. If the exchange holding your short position (or long, depending on your setup) sees your collateral drop below the maintenance requirement, you get liquidated. This happens even if your other position is profitable. The profit from the hedge might not arrive in time to save you. This is why proper margin management is not optional; it is the difference between a small loss and a wiped account.

Basis risk

Basis risk occurs when the price of the futures contract and the spot price do not move in perfect lockstep. In an ideal world, the spread between the two would be predictable. In reality, market sentiment can cause the futures price to diverge significantly from the spot price. If you are relying on the convergence of these two prices to close your position profitably, a widening spread can eat into your profits or turn a winning trade into a loser. This is especially common during periods of high volatility or market stress, when the "arbitrage" opportunity disappears as quickly as it appeared.

Smart contract risk

If you are executing funding rate arbitrage on decentralized exchanges or using DeFi protocols for your hedging, you are exposed to smart contract risk. These are the underlying codebases that manage your funds. If there is a bug, a vulnerability, or even a successful hack, your funds can be drained. Unlike centralized exchanges, there is often no customer support to call and no insurance fund to reimburse you. You are relying entirely on the security of the code. This risk is real and significant, particularly in newer or less audited protocols.

How to execute a funding arb trade

Executing a funding arb trade is less about predicting price direction and more about capturing the spread between borrowing costs and lending yields. The core mechanic is simple: you hold a long spot position to collect funding payments while simultaneously holding a short perpetual futures position to hedge against market volatility. This creates a delta-neutral setup where your profit comes from the periodic funding rate payments, not from the asset's price movement.

1. Identify high-yield assets

Start by scanning the market for tokens with consistently positive funding rates. You want assets where the demand for long positions is high enough to pay short sellers regularly. Use a data aggregator like Coinglass or WunderTrading to filter for coins with funding rates above the baseline. Look for stability over time rather than one-off spikes, as consistent rates reduce the risk of the spread closing before you can exit.

Look for tokens with positive funding rates that have held steady over the last 24-48 hours. Avoid assets with erratic spikes, as these often signal temporary market stress rather than sustainable yield. Prioritize liquid markets to ensure you can enter and exit positions without significant slippage.

2. Calculate the risk-reward ratio

Before opening any positions, run the numbers. Your potential profit is the funding rate minus trading fees and funding fees. You must account for the exchange's trading fees on both the spot and futures legs, as well as the cost of borrowing if you are using leverage. If the annualized funding rate doesn't comfortably exceed these costs plus a buffer for potential liquidation risk, the trade may not be worth the capital allocation.

3. Open hedged positions

Execute the trade by buying the asset on the spot market and shorting the same amount on the perpetual futures market. Most traders use cross-margin mode to share collateral between the two positions, which helps prevent liquidation on one side if the price moves sharply. Ensure the notional values of both positions are equal to maintain a delta-neutral stance.

Buy the asset on the spot market and simultaneously open an equal-sized short position on the perpetual futures contract. Use cross-margin mode to share collateral between the two legs, which provides a buffer against price volatility. Verify that the notional values match exactly to ensure you are truly delta-neutral.

4. Monitor and rebalance

Once the positions are open, the work isn't done. You need to monitor the funding rate to ensure it remains positive and sufficient to cover your costs. If the rate drops below your threshold, consider closing the position. Additionally, rebalance your hedge if the price moves significantly and the value of your spot and futures positions drift apart. This ensures your delta-neutral status is maintained.

Check your positions regularly to ensure the funding rate remains profitable. Rebalance your hedge if the price moves significantly and the value of your spot and futures positions drift apart. This ensures your delta-neutral status is maintained and prevents unintended exposure to market risk.

Frequently asked questions about funding arb

How do I calculate the annualized yield of a funding rate?

To calculate the annualized yield, multiply the periodic funding rate by the number of funding intervals in a year. Since most major exchanges pay funding every 8 hours, there are 3 intervals per day and 1,095 intervals per year. For example, a 0.01% funding rate every 8 hours results in an annualized yield of approximately 10.95% (0.01% * 1,095), before accounting for trading fees and slippage.

What is the minimum capital required to start funding arb?

The minimum capital depends on the exchange's minimum order size and margin requirements. On most centralized exchanges, you can start with as little as $50-$100 worth of crypto, provided the exchange allows fractional trading. However, smaller positions are more susceptible to being eaten alive by fixed trading fees (maker/taker fees), so a larger capital base (e.g., $500+) is often recommended to achieve meaningful net returns.

Can I lose money if the market crashes?

Yes. While funding arb is market-neutral, it is not immune to liquidation. If the market crashes sharply, the value of your spot holdings drops. If your short position is on a different exchange or uses segregated margin, you might not have enough collateral to cover the loss, leading to liquidation. Even with unified margin, a sudden drop can trigger a margin call if you haven't maintained a sufficient safety buffer above the maintenance margin requirement.

No comments yet. Be the first to share your thoughts!