How funding rate arbitrage works

Funding rate arbitrage captures periodic payments between long and short traders on perpetual futures. Unlike directional trading, this strategy profits from the spread between funding rates on different exchanges, not price movement.

Perpetual futures lack expiration dates. To keep the futures price tethered to the spot price, exchanges use funding payments. When futures trade above spot, longs pay shorts. When below, shorts pay longs. These payments typically occur every eight hours.

Arbitrageurs exploit discrepancies in these rates across venues. The core mechanism involves taking a long position on spot (or a low-funding futures market) while simultaneously shorting a high-funding futures market. This pairing creates a delta-neutral position, insulating the trader from price volatility.

By balancing these opposing positions, the strategy isolates the yield component. Traders monitor funding rates to ensure the spread remains wide enough to cover transaction costs, such as trading fees and withdrawal fees, while maintaining a hedge against market swings.

Cex vs dex funding arb choices that change the plan

Funding rate arbitrage relies on capturing the spread between spot and perpetual markets, but the infrastructure you choose dictates your actual returns. Centralized exchanges (CEX) and decentralized exchanges (DEX) offer fundamentally different risk-reward profiles.

Liquidity and Execution

Liquidity determines how much capital you can deploy without slippage. CEXs like Binance and Bybit aggregate order books from thousands of traders, resulting in tight spreads and high depth. This allows for large position sizes with minimal price impact. DEXs, particularly on Ethereum, rely on automated market makers (AMMs). While newer DEXs have improved, their liquidity pools are often fragmented. Large trades on DEXs can significantly move the price, eroding the funding rate profit.

Execution speed is also critical. Funding rates are typically settled every 8 hours on CEXs. To capture the spread, you need to enter positions quickly before the rate resets. CEXs offer sub-second trade execution. DEXs depend on blockchain block times and gas prices. During high network congestion, transactions can be delayed or fail entirely, causing you to miss the funding window or pay excessive fees.

Fees and Counterparty Risk

CEX trading fees are generally lower for high-volume traders due to maker-taker models. However, you must also consider withdrawal fees and the risk of exchange insolvency. When you deposit funds on a CEX, you surrender custody. Historical events like the FTX collapse demonstrate that counterparty risk is a real threat to funding arb strategies.

DEXs eliminate counterparty risk because you trade directly from your wallet using smart contracts. You retain custody of your assets at all times. However, DEX fees can be prohibitive. Ethereum gas fees can range from $5 to $50+ per transaction. For smaller positions, these fees can exceed the funding rate profit. Additionally, smart contract risk exists; bugs or exploits in the DEX protocol could lead to loss of funds.

Comparison Overview

The following table summarizes the key differences between CEX and DEX funding arbitrage.

| Feature | Centralized Exchange (CEX) | Decentralized Exchange (DEX) |

|---|---|---|

| Liquidity | High, deep order books | Variable, often fragmented |

| Execution Speed | Sub-second | Block-time dependent |

| Fees | Low trading fees, withdrawal costs | High gas fees, protocol fees |

| Custody | Exchange holds funds | Self-custody |

| Counterparty Risk | High (exchange insolvency) | Low (smart contract risk) |

Which is Right for You?

For large capital deployments, CEXs are often necessary due to their liquidity. The ability to enter and exit large positions without slippage is paramount. However, you must carefully select exchanges with strong regulatory compliance and transparent reserves. For smaller accounts or those prioritizing security, DEXs offer a safer custody model. The key is to calculate whether the funding rate spread justifies the higher gas fees and potential slippage on DEXs.

Capital Efficiency and Leverage Risks

Funding arbitrage is often marketed as a low-risk strategy, but this reputation hides the dangers of leverage. While research indicates that funding rate arbitrage can exhibit lower volatility than directional trading, it is not immune to liquidation events. The core tension lies in capital efficiency: using leverage amplifies returns from small funding rate differentials, but it also compresses the margin of safety against price swings.

When you trade with leverage, you are borrowing capital to increase your position size. If the underlying asset moves against your hedge, the exchange will liquidate your position before you can recover. This risk is acute in decentralized finance (DeFi) where smart contract bugs or oracle failures can trigger sudden, unanticipated liquidations. In centralized exchanges (CEX), the risk is primarily market-driven, but the mechanics of margin calls remain unforgiving.

The Cost of Borrowed Money

Leverage is not free. When you use borrowed funds, you pay interest on the loan. In a funding arbitrage setup, you must ensure that the funding rate income exceeds the cost of borrowing. If the funding rate drops or turns negative, your costs can eat into your principal. This dynamic requires constant monitoring and adjustment of positions.

Liquidation Mechanics

Liquidation occurs when your account equity falls below the maintenance margin requirement. In a leveraged funding arbitrage trade, this can happen if:

- The spot price moves sharply against your short position (if you are shorting the perpetual and holding spot).

- The funding rate reverses, turning your expected income into a cost.

- Exchange maintenance margin requirements increase during high volatility.

Managing Risk

To mitigate these risks, traders often use lower leverage ratios (e.g., 2x-5x) rather than high leverage (10x+). This provides a larger buffer against price swings. Additionally, diversifying across multiple exchanges and assets can reduce exposure to a single point of failure. Always calculate your liquidation price before entering a trade and set strict stop-loss orders where possible.

Tracking rates with technical analysis

Funding rates are not random; they are the market's price for leverage. When traders pile into long positions, the rate spikes positive. When they short heavily, it turns negative. Technical analysis helps you spot these imbalances before they peak, allowing you to enter arbitrage positions when the spread is widest.

Start by overlaying funding rate data on price charts. Most professional terminals allow you to plot the 8-hour or daily funding rate alongside the asset's price. Look for divergence. If the price is making new highs but funding rates are starting to flatten or drop, the rally may be losing momentum. Conversely, if the price is dropping but funding rates are becoming deeply negative, a short squeeze could be imminent.

Focus on historical spikes during high volatility. During market crashes or parabolic rallies, funding rates can exceed 1% per 8 hours. These spikes are short-lived. Use moving averages or Bollinger Bands on the funding rate chart itself to identify when the rate is statistically extreme relative to its recent history. Entering when the rate is two standard deviations above the mean often provides the best risk-adjusted return.

Use the

to visualize the relationship between price action and volume. While this chart shows price, correlate it with a separate funding rate feed from your exchange. When volume surges alongside extreme funding rates, the trend is likely overextended. This is your signal to open the arbitrage position, betting that the rate will revert to the mean as the leverage flushes out.Steps to execute your first trade

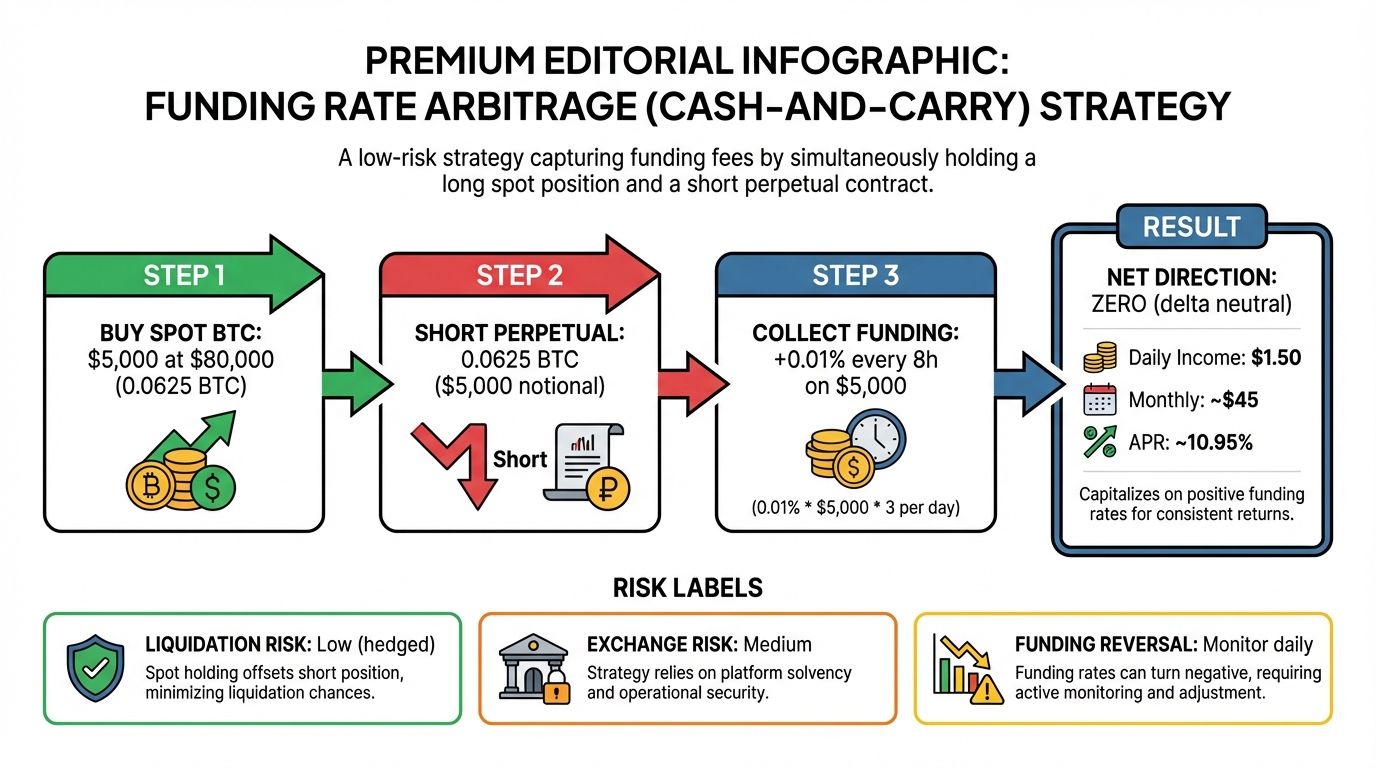

Funding arbitrage relies on capturing the spread between spot and perpetual futures markets. The core mechanism involves holding a long position on an exchange with low or negative funding rates while simultaneously shorting the same asset on an exchange with high positive rates. This structure locks in the funding payments as profit, regardless of the asset's price direction.

Select two reputable centralized exchanges (CEXs) with high liquidity for your target asset. Compare their current funding rates using a data provider like CoinGlass or Coinglass. You need a significant spread—typically above 0.1% per 8 hours—to cover trading fees and still generate a net profit. Ensure both platforms support the same trading pairs and have sufficient depth to enter your positions without slippage.

Transfer your capital to the exchange with the lower funding rate. Purchase the target asset (e.g., BTC or ETH) using stablecoins or the native currency. Hold this asset in your spot wallet. This long position acts as your hedge; if the market price rises, the value of your spot holdings increases, offsetting potential losses on your short futures position.

Move the equivalent amount of the asset to the exchange with the higher funding rate. Open a perpetual futures short position with the same notional value as your spot holdings. For example, if you bought $10,000 worth of BTC on Exchange A, short $10,000 worth of BTC on Exchange B. Use 1x leverage to maintain a delta-neutral profile. This short position earns you the high funding payments every 8 hours.

Track your positions daily. While the strategy is market-neutral, you face exchange-specific risks like withdrawal halts, API failures, or sudden changes in funding rates. Ensure you have enough margin on the short side to avoid liquidation if the market moves sharply against your short position. Set up alerts for funding rate drops or unusual volatility. Rebalance your positions if the spread narrows significantly or if one exchange imposes restrictions.

Common funding arb mistakes to avoid

Funding rate arbitrage looks simple on paper: go long spot, short futures, and collect the spread. In practice, execution friction and hidden costs often eat into those profits. Even experienced traders stumble over timing, liquidity traps, and protocol risks.

Ignoring funding payment timing

The funding interval varies by exchange. Binance and Bybit charge every eight hours, while others may use hourly or four-hour cycles. If you open a position just before a payment window, you might pay the fee immediately without enough time for the price action to work in your favor. Always check the exact settlement schedule before entering.

Overlooking withdrawal delays

When moving funds between centralized exchanges (CEX) and decentralized finance (DeFi) protocols, network congestion can cause significant delays. A withdrawal stuck in the mempool means your hedge isn’t live, leaving you exposed to market swings. Buffer your capital to account for potential network delays, especially during high-traffic periods.

Underestimating smart contract risk

DeFi funding arbitrage relies on smart contracts to manage positions and distribute payments. Unlike CEXs, there is no customer support or insurance fund to recover funds if a protocol is exploited or fails. Audit reports are not guarantees. Only allocate capital you are willing to lose entirely to protocol-specific risks.

Chasing low-liquidity pairs

High funding rates often appear on low-volume altcoins. While the spread looks attractive, the bid-ask spread and slippage can be substantial. Exiting a position in a thin market may cost more than the funding payment itself. Stick to pairs with deep order books to ensure you can enter and exit without moving the price.

No comments yet. Be the first to share your thoughts!