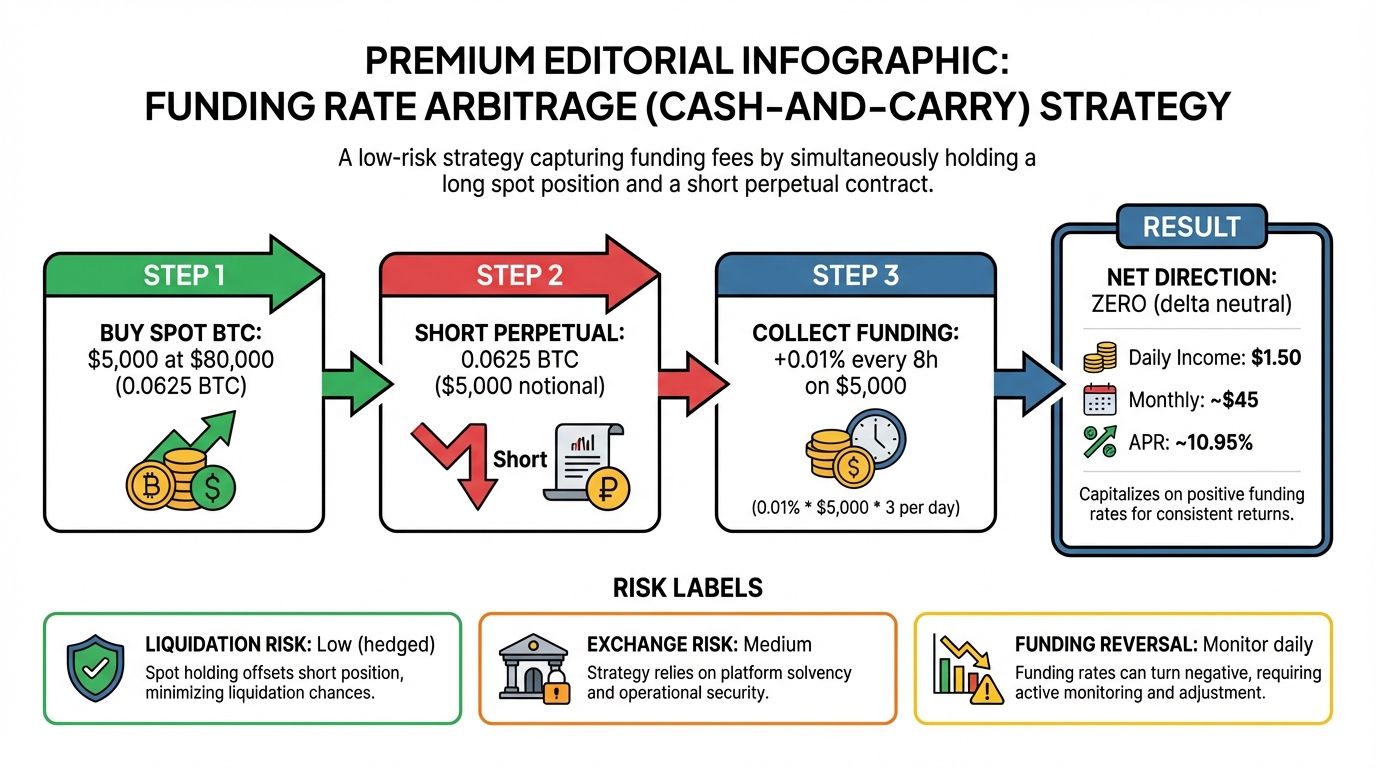

What is funding rate arbitrage

Funding rate arbitrage is a delta-neutral strategy that allows you to earn income from the difference in funding fees without depending on the direction of asset price movement. You achieve this by holding opposite positions in the spot and perpetual futures markets for the same trading pair. When the funding rate is positive, you buy the asset on the spot market and short it on the futures market, collecting the periodic payments from traders who are long.

This approach effectively neutralizes directional price risk. If Bitcoin spikes in price, your spot holdings gain value while your short futures position loses an equivalent amount, leaving your net exposure flat. Your profit comes solely from the funding rate differential, which acts as a yield on your capital. This mechanism is particularly attractive in bull markets where long positions dominate and are willing to pay a premium to maintain leverage.

The strategy relies on the structural design of perpetual swaps, which lack an expiration date. To keep the futures price tethered to the spot price, exchanges charge a funding fee every few hours. If the futures price trades above the spot price, longs pay shorts. By positioning yourself as the short side in the futures market while holding the underlying asset in spot, you become the recipient of these payments.

Understanding this dynamic is essential before executing a funding arb strategy. While the concept seems straightforward, the actual returns depend on the spread between the funding rate and your trading fees. You must account for exchange fees, slippage, and the cost of borrowing if you are using margin. The goal is to capture the spread after all costs are deducted, ensuring that the yield generated by the funding rate exceeds the friction of the trade.

Step 1: Select exchanges with rate divergence

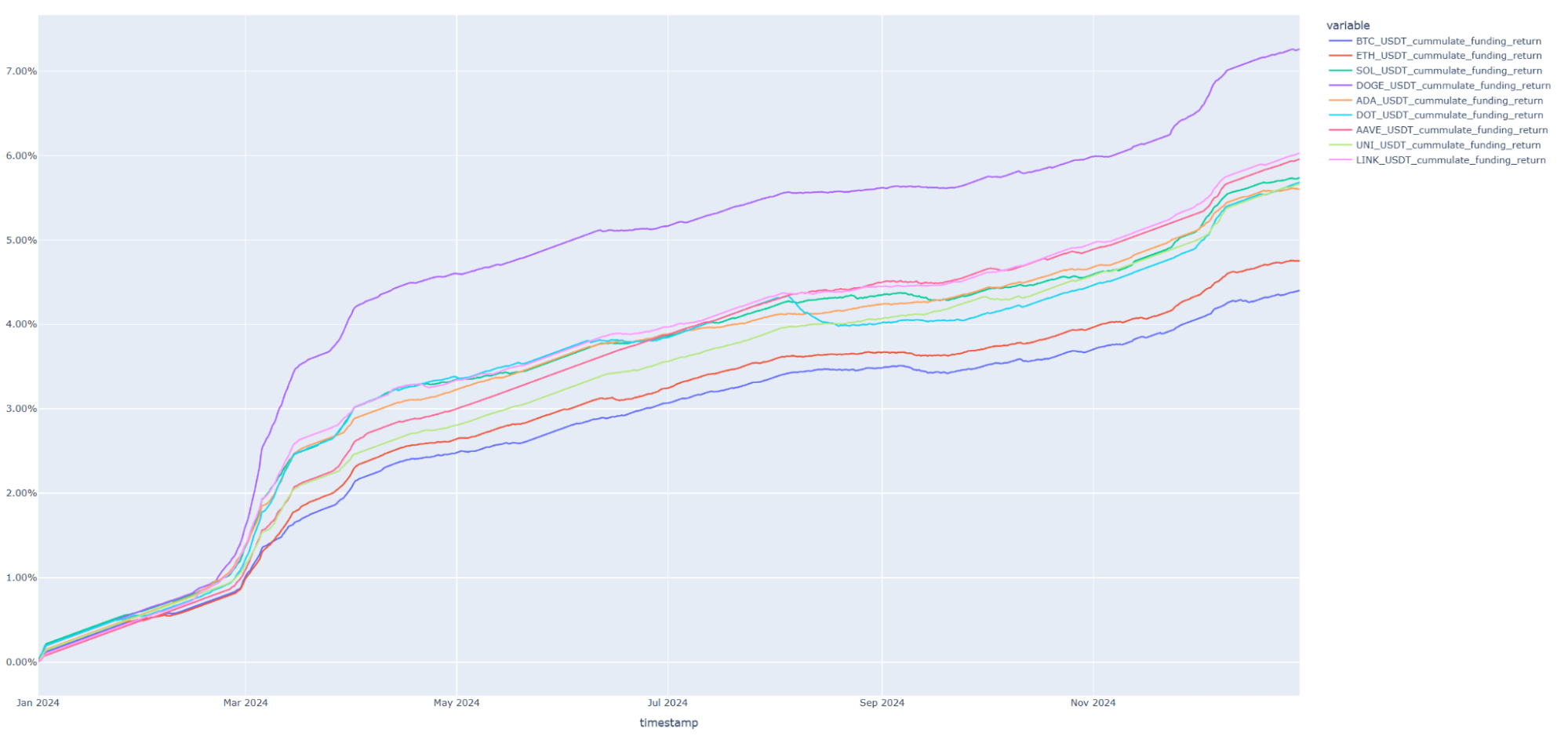

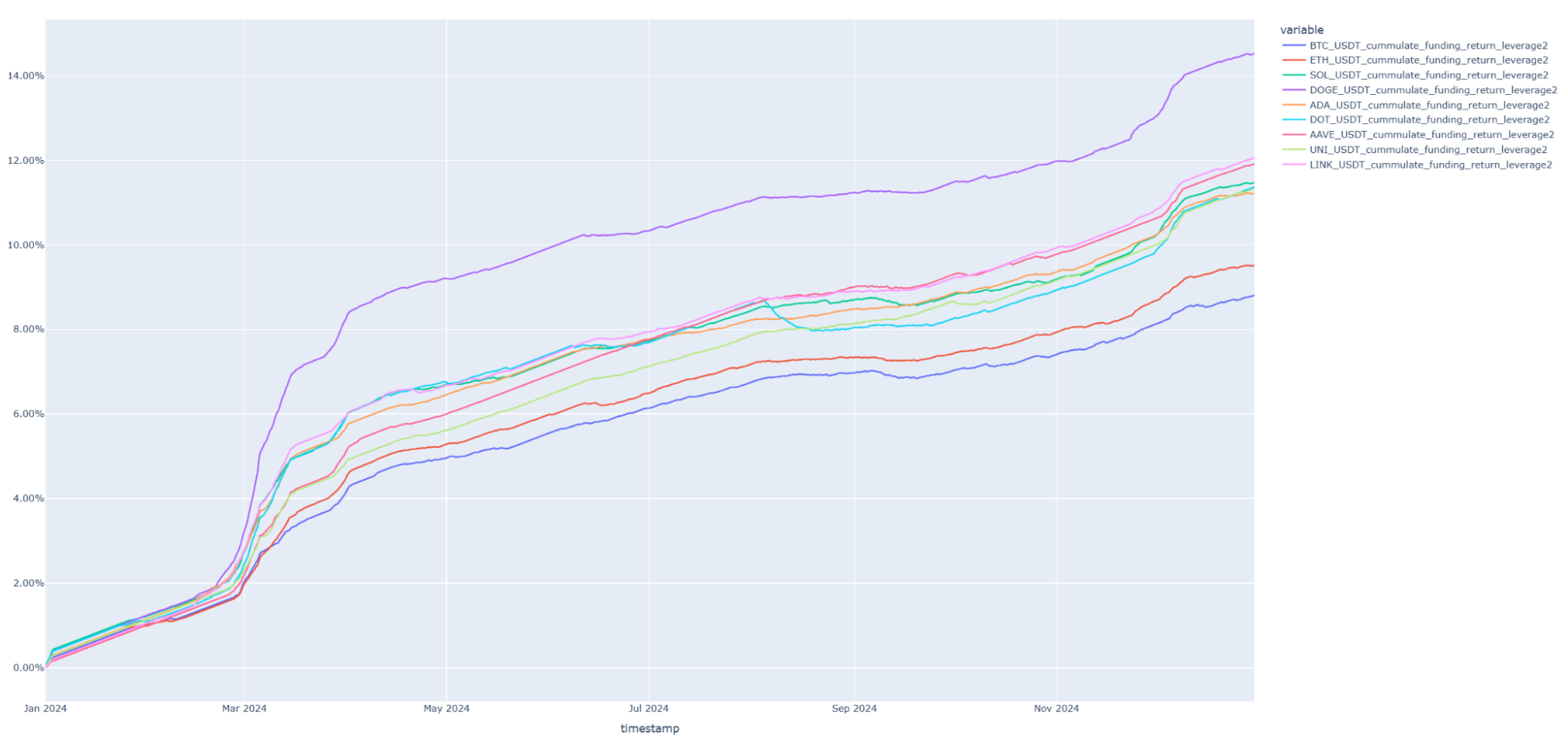

A funding arb strategy only works if you can find two venues where the spread is wide enough to cover fees and risk. You aren't looking for a fleeting spike; you need a structural divergence that persists across multiple funding intervals. Most retail traders check a single snapshot and miss the decay, but serious arbitrage requires looking at historical trends and regime shifts.

Start by monitoring the perpetual swap markets on major centralized exchanges. Look for pairs where one exchange is pricing future demand significantly higher than another. For example, if Binance shows a positive funding rate of 0.01% while Bybit shows -0.005%, you have a spread. The goal is to identify this gap before the market corrects itself.

Use aggregators or direct exchange APIs to monitor funding rates for BTC and ETH across Binance, Bybit, OKX, and others. Filter for positive rates on one side and negative or lower positive rates on the other. A consistent spread of 0.01% or more per 8 hours is a strong candidate.

Don't rely on a single data point. Check the 30-day average funding rate for your selected pair. If the spread is wide only during extreme volatility, it may not be sustainable for a delta-neutral hold. Look for steady, structural differences in how each exchange prices leverage demand.

Before committing capital, confirm that you can move funds between the two exchanges quickly and cheaply. Some exchanges have high minimums or slow withdrawal times that can erase your profit margin. Ensure your chosen venues support the trading pairs you identified.

The key is patience. A funding arb strategy is about capturing small, reliable yields over time, not hitting a home run. If the spread looks too good to be true, it probably is. Stick to major exchanges with deep liquidity to minimize slippage risk.

Step 2: Calculate the net yield after fees

To execute a funding arb strategy effectively, define the constraint first, compare realistic options, test the tradeoff, and choose the path with the fewest hidden costs. This sequence keeps the advice usable.

After each step, pause to check whether the recommendation fits your actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Execute the delta-neutral position

This is where the theory meets the order book. You are no longer analyzing; you are acting. The goal here is to lock in the funding rate spread by creating a perfectly balanced portfolio: long spot, short futures. If the hedge ratio is off, you aren't arbitraging; you're gambling on direction.

Follow this sequence exactly. Speed matters, but precision matters more. One wrong click on the futures side and your delta-neutral status vanishes.

Start by buying the underlying asset on the spot market. Use a limit order slightly below the current market price to reduce slippage, or a market order if you need immediate liquidity. This position is your anchor. It gives you the actual coins that will earn the funding payments.

Immediately open a short position on the futures market for the same trading pair. This is the hedge. By shorting, you neutralize the price risk of your spot holdings. If the price crashes, your spot loses value but your short gains. If the price rallies, your spot gains but your short loses. The net PnL from price movement is zero.

Check your position sizes. If you bought 1 BTC on spot, you must short 1 BTC on futures. Many platforms allow leverage, but for a true delta-neutral funding arb strategy, you want 1x leverage on the short side. Higher leverage introduces liquidation risk that destroys the safety of the arbitrage. Ensure the notional values match exactly.

The mechanics are simple, but the execution requires discipline. Funding payments are typically distributed every 8 hours. Your position must remain open and balanced through these intervals. If you close the spot position but forget to close the futures, you are no longer hedged. You are now exposed to directional market risk.

Keep your margin requirements in mind. While the position is delta-neutral, exchange maintenance margins still apply. Ensure you have enough collateral in the futures account to prevent liquidation during temporary volatility spikes. A liquidated short position wipes out the arbitrage profit instantly.

Manage liquidation and basis risk

The funding arb strategy looks safe on paper because you hold equal and opposite positions in spot and futures. In practice, the market does not move in straight lines. If volatility spikes, your positions can drift apart, creating two distinct threats: liquidation of your futures leg and basis risk eroding your hedge.

Protecting against liquidation

Liquidation happens when the margin in your futures account drops below the maintenance threshold. Even though your spot position offsets the price risk, the exchange only sees the futures account balance. If the market moves sharply against your short futures position, you need enough cash or collateral to stay alive.

Most traders keep their margin ratio well above the minimum requirement. A common practice is to maintain at least 1.5x to 2x the initial margin requirement. This buffer absorbs temporary price swings without triggering a forced close. You should also monitor the funding rate closely; if it spikes, the cost of holding the short position increases, which can eat into your available margin if you are not careful.

Managing basis risk

Basis risk is the difference between the spot price and the futures price. In a funding arb, you profit from the funding rate, but you are exposed to changes in the basis. If the futures price drops below the spot price (backwardation), your short futures position loses value relative to your spot holding.

This risk is real even when funding is positive. As Blockhouse notes, a serious strategy cannot rely on snapshots; it requires predictive analysis across market regimes. If the basis narrows or flips, your hedge becomes less effective. You should track the basis spread regularly and be prepared to adjust your position size or close the trade if the basis moves against you significantly.

Practical steps

- Monitor margin levels daily. Set alerts for when your margin ratio drops below 1.5x.

- Track the basis spread. Use a reliable data source to watch the difference between spot and futures prices.

- Adjust position sizes. If the basis widens unfavorably, consider reducing your futures position to lower exposure.

- Stay informed. Follow market news and funding rate trends to anticipate shifts in market sentiment.

No comments yet. Be the first to share your thoughts!